Begun, the Wallet Wars, have.

October 27, 2014 9:56 AM Subscribe

Apple recently launched Apple Pay, a contactless payment system that uses NFC, tokenization, and TouchID for an easy and secure payment experience. Now retailers like CVS and Rite Aid are turning off their NFC support to lock out Apple Pay (and other payments systems that use NFC such as Google Wallet). Why?

The usual reasons. A consortium of retailers, including Walmart, Target, Best Buy, CVS, Rite Aid, and many others, plans to introduce CurrenC, a rival payment system, next year. The goal is to eliminate credit card processing fees while continuing to gather tons of information on their customers. Members of the consortium must sign three-year mobile payment app exclusivity deals with MCX. This is uniting some previously disparate factions.

Their, uh, interesting method of implementation involves QR codes, your bank account, driver's license, and SSN (screenshot). That's okay though, what could go wrong?

The usual reasons. A consortium of retailers, including Walmart, Target, Best Buy, CVS, Rite Aid, and many others, plans to introduce CurrenC, a rival payment system, next year. The goal is to eliminate credit card processing fees while continuing to gather tons of information on their customers. Members of the consortium must sign three-year mobile payment app exclusivity deals with MCX. This is uniting some previously disparate factions.

Their, uh, interesting method of implementation involves QR codes, your bank account, driver's license, and SSN (screenshot). That's okay though, what could go wrong?

{kind=link}

This is asinine. ACH is not intended for direct point payments, and the infrastructure around it won't treat it that way. In a year, you will see this crap listed as a reason for massive losses at these retailers.

posted by sonic meat machine at 9:59 AM on October 27, 2014 [18 favorites]

posted by sonic meat machine at 9:59 AM on October 27, 2014 [18 favorites]

You know, it's not that big a inconvenience to me to run by the ATM on the way to the store, much less than trying to sort this out.

posted by T.D. Strange at 10:01 AM on October 27, 2014 [7 favorites]

posted by T.D. Strange at 10:01 AM on October 27, 2014 [7 favorites]

There are plenty of places that now accept Apple Pay (Walgreen's/Duane Reade) that already collect your information. Apple Pay does not protect you from that.

posted by roomthreeseventeen at 10:02 AM on October 27, 2014

posted by roomthreeseventeen at 10:02 AM on October 27, 2014

Even weirder: sometimes you have to scan their QR code, and sometime you have to show them one on your device. Which to me only makes it even more confusing!

posted by wenestvedt at 10:02 AM on October 27, 2014

posted by wenestvedt at 10:02 AM on October 27, 2014

roomthreeseventeen, I agree: unless Apple Pay deprives the seller of the use of a loyalty card, what are they losing?

posted by wenestvedt at 10:03 AM on October 27, 2014

posted by wenestvedt at 10:03 AM on October 27, 2014

Will Apple be able to swap out their NFC chip for an EMV chip once chip-and-pin rolls out?

posted by mullacc at 10:04 AM on October 27, 2014

posted by mullacc at 10:04 AM on October 27, 2014

Also, the app wants access to your health data. (source)

It's really a shopper's dream. Just:

It's really a shopper's dream. Just:

- unlock your phone

- open the CurrentC app

- select "pay"

- scan the store QR code

- let the cashier scan your QR code

- have the money be deducted from your checking account with limited fraud protection

- let that store and every other store in the consortium track and share all your purchases

- oh and also your health information

There are plenty of places that now accept Apple Pay (Walgreen's/Duane Reade) that already collect your information. Apple Pay does not protect you from that.

Do you mean they collect info via Apple Pay?

posted by mullacc at 10:05 AM on October 27, 2014

Do you mean they collect info via Apple Pay?

posted by mullacc at 10:05 AM on October 27, 2014

CurrentC not CurrenC.

ACH also provides no consumer level protection against fraud.

I've had my card compromised four times in the last two years. I am done with credit cards. So Apple Pay intrigues me, but when people make it difficult for me to pay them I generally don't.

Apple Pay does protect you from data gathering, since it doesn't use a trackable number. Each transaction has its own number. No coupons, special offers, or other stupid clutter.

posted by cjorgensen at 10:05 AM on October 27, 2014 [5 favorites]

ACH also provides no consumer level protection against fraud.

I've had my card compromised four times in the last two years. I am done with credit cards. So Apple Pay intrigues me, but when people make it difficult for me to pay them I generally don't.

Apple Pay does protect you from data gathering, since it doesn't use a trackable number. Each transaction has its own number. No coupons, special offers, or other stupid clutter.

posted by cjorgensen at 10:05 AM on October 27, 2014 [5 favorites]

I've been reading about this everywhere. QR codes...AHAHAHAHAHAAAHHAHAAHHHAAAAA!!!

The weird thing is that most of those retailers had NFC implemented and ApplePay was working with them. Then, seemingly overnight, they all pulled the plug on NFC.

I'm thinking that MCX quietly reminded the retailers that they had a contractual obligation to use CurrentC and they should cease and desist using NFC. Or el$e.

posted by Thorzdad at 10:05 AM on October 27, 2014 [1 favorite]

The weird thing is that most of those retailers had NFC implemented and ApplePay was working with them. Then, seemingly overnight, they all pulled the plug on NFC.

I'm thinking that MCX quietly reminded the retailers that they had a contractual obligation to use CurrentC and they should cease and desist using NFC. Or el$e.

posted by Thorzdad at 10:05 AM on October 27, 2014 [1 favorite]

Will prices drop because of this new payment method ? Since the stores are saving on the credit card fees, they should split the difference.. Oh, wait, what am I smoking ?

posted by k5.user at 10:06 AM on October 27, 2014 [18 favorites]

posted by k5.user at 10:06 AM on October 27, 2014 [18 favorites]

As far as I know, almost all stores accept cash. Just sayin'

posted by double block and bleed at 10:06 AM on October 27, 2014 [7 favorites]

posted by double block and bleed at 10:06 AM on October 27, 2014 [7 favorites]

Former Walmart CEO Lee Scott has reportedly said: "I don’t know that MCX will succeed, and I don’t care. As long as Visa suffers."

posted by 1970s Antihero at 10:06 AM on October 27, 2014 [2 favorites]

posted by 1970s Antihero at 10:06 AM on October 27, 2014 [2 favorites]

What? I have been using Google Wallet at CVS for months now. Just...ugh. Ugh. What utter tools.

posted by selfnoise at 10:06 AM on October 27, 2014 [4 favorites]

posted by selfnoise at 10:06 AM on October 27, 2014 [4 favorites]

I have a feeling Apple will just block the CurrentC app from the App Store. Seems only fair if they're blocking Apple Pay from their stores.

posted by the jam at 10:06 AM on October 27, 2014 [24 favorites]

posted by the jam at 10:06 AM on October 27, 2014 [24 favorites]

Do you mean they collect info via Apple Pay?

No, I meant that just because you're using Apple Pay doesn't mean the store cares about your privacy.

posted by roomthreeseventeen at 10:07 AM on October 27, 2014

No, I meant that just because you're using Apple Pay doesn't mean the store cares about your privacy.

posted by roomthreeseventeen at 10:07 AM on October 27, 2014

Also, the app wants access to your health data. (source)

It's really a shopper's dream. Just:

unlock your phone

open the CurrentC app

select "pay"

scan the store QR code

let the cashier scan your QR code

have the money be deducted from your checking account with limited fraud protection

let that store and every other store in the consortium track and share all your purchases

oh and also your health information

Was this a result of some sort of challenge to make BitCoin actually look good by comparison?

posted by Drinky Die at 10:07 AM on October 27, 2014 [74 favorites]

It's really a shopper's dream. Just:

unlock your phone

open the CurrentC app

select "pay"

scan the store QR code

let the cashier scan your QR code

have the money be deducted from your checking account with limited fraud protection

let that store and every other store in the consortium track and share all your purchases

oh and also your health information

Was this a result of some sort of challenge to make BitCoin actually look good by comparison?

posted by Drinky Die at 10:07 AM on October 27, 2014 [74 favorites]

There are plenty of places that now accept Apple Pay (Walgreen's/Duane Reade) that already collect your information. Apple Pay does not protect you from that.

ApplePay, itself, does not collect information. Nor does it share any information. It just validates your credit or debit card.

CurrentC is all about information collection and distribution of that information among its members, whether you shop at them or not, and scant little else.

posted by Thorzdad at 10:08 AM on October 27, 2014 [3 favorites]

ApplePay, itself, does not collect information. Nor does it share any information. It just validates your credit or debit card.

CurrentC is all about information collection and distribution of that information among its members, whether you shop at them or not, and scant little else.

posted by Thorzdad at 10:08 AM on October 27, 2014 [3 favorites]

Considering how badly the interface for checkout using a credit card at walgreens/cvs is already, it doesn't surprise me that they'd be upping their shitty checkout game to new levels.

posted by Ferreous at 10:10 AM on October 27, 2014 [4 favorites]

posted by Ferreous at 10:10 AM on October 27, 2014 [4 favorites]

Congratulations to MCX for making Apple look open and Google privacy oriented. They need to work on their relationship with Facebook users to score a trifecta.

posted by Bovine Love at 10:10 AM on October 27, 2014 [24 favorites]

posted by Bovine Love at 10:10 AM on October 27, 2014 [24 favorites]

Also, Verizon and the other cell phone providers are pushing Softcard which is NFC based. So these retailers have now pissed off:

-The major cell phone ISPs

-Google

-Apple

Good luck with that, you miserable idiots.

posted by selfnoise at 10:10 AM on October 27, 2014 [11 favorites]

-The major cell phone ISPs

-Apple

Good luck with that, you miserable idiots.

posted by selfnoise at 10:10 AM on October 27, 2014 [11 favorites]

There are plenty of places that now accept Apple Pay (Walgreen's/Duane Reade) that already collect your information. Apple Pay does not protect you from that.

Those places ask for both your driver's license number and Social Security number?

posted by grubi at 10:10 AM on October 27, 2014 [1 favorite]

Those places ask for both your driver's license number and Social Security number?

posted by grubi at 10:10 AM on October 27, 2014 [1 favorite]

We are the product!!!

posted by ZenMasterThis at 10:11 AM on October 27, 2014 [2 favorites]

I want to try CurrentC but I haven't been able to figure out how to plug this CueCat into my phone.

posted by komara at 10:11 AM on October 27, 2014 [122 favorites]

posted by komara at 10:11 AM on October 27, 2014 [122 favorites]

I have a feeling Apple will just block the CurrentC app from the App Store. Seems only fair if they're blocking Apple Pay from their stores.

posted by the jam at 1:06 PM on October 27 [+] [!]

Yeah, they seem to think Apple is going to put it in the app store:

The CurrentC mobile wallet app will be free to download through both the App StoreSM and Google PlayTM store, and is compatible with major smartphones.

posted by R. Mutt at 10:11 AM on October 27, 2014 [5 favorites]

posted by the jam at 1:06 PM on October 27 [+] [!]

Yeah, they seem to think Apple is going to put it in the app store:

The CurrentC mobile wallet app will be free to download through both the App StoreSM and Google PlayTM store, and is compatible with major smartphones.

posted by R. Mutt at 10:11 AM on October 27, 2014 [5 favorites]

I think it would behoove Apple to allow it in the App Store. Let people go through all those steps and then say "See? Apple Pay isn't that intrusive or that big of a deal."

posted by grubi at 10:13 AM on October 27, 2014 [3 favorites]

posted by grubi at 10:13 AM on October 27, 2014 [3 favorites]

As far as I know, almost all stores accept cash. Just sayin'

Actually I've been in several restaurants that don't accept cash. Card only or go elsewhere. And try paying for something with cash in an Apple store. Sure, you can do it, but it's a pain compared to cash (or their store app).

You know, it's not that big a inconvenience to me to run by the ATM on the way to the store, much less than trying to sort this out.

You mean the ATM that wasn't to charge me $2.50 to get out $20? or do you mean the one that's on the other side of town that my bank let's me use for free?

This is also a bit tiresome. We get it, you cash guys don't see the point. You're probably also happy with your flip phone.

posted by cjorgensen at 10:13 AM on October 27, 2014 [21 favorites]

Actually I've been in several restaurants that don't accept cash. Card only or go elsewhere. And try paying for something with cash in an Apple store. Sure, you can do it, but it's a pain compared to cash (or their store app).

You know, it's not that big a inconvenience to me to run by the ATM on the way to the store, much less than trying to sort this out.

You mean the ATM that wasn't to charge me $2.50 to get out $20? or do you mean the one that's on the other side of town that my bank let's me use for free?

This is also a bit tiresome. We get it, you cash guys don't see the point. You're probably also happy with your flip phone.

posted by cjorgensen at 10:13 AM on October 27, 2014 [21 favorites]

On the plus side, I guess you could go and sign up a secondary bank account and link it to CurrentC so that you're eligible for the inevitable class action lawsuit settlement.

posted by sonic meat machine at 10:13 AM on October 27, 2014 [44 favorites]

posted by sonic meat machine at 10:13 AM on October 27, 2014 [44 favorites]

This is the sort of thing that actually makes me care about distributed cryptocurrencies. I don't much care for anarcholibertarianism, but it beats panopticon capitalism (except where it's equivalent).

posted by weston at 10:13 AM on October 27, 2014 [8 favorites]

posted by weston at 10:13 AM on October 27, 2014 [8 favorites]

I honestly don't know why anyone would support middlemen in payment processes, be it one or some combination of credit cards, Apple Pay, or this monstrosity. As consumers we always pay for this stuff, and I refuse to play the "which corp do I get angry at" game when it's just one corp's P&L versus another's. Technology is supposed to enable disintermediation.

posted by sylvanshine at 10:14 AM on October 27, 2014 [6 favorites]

posted by sylvanshine at 10:14 AM on October 27, 2014 [6 favorites]

CVS is already the absolute worst on privacy protection.

Anything that gives them more data is a bad idea.

posted by mercredi at 10:15 AM on October 27, 2014 [6 favorites]

Anything that gives them more data is a bad idea.

posted by mercredi at 10:15 AM on October 27, 2014 [6 favorites]

Actually I've been in several restaurants that don't accept cash. Card only or go elsewhere.

If they're billing you after the meal, that could be illegal - there's a reason our currency is marked "legal tender for all debts public and private".

posted by NoxAeternum at 10:17 AM on October 27, 2014 [36 favorites]

If they're billing you after the meal, that could be illegal - there's a reason our currency is marked "legal tender for all debts public and private".

posted by NoxAeternum at 10:17 AM on October 27, 2014 [36 favorites]

One of the things that always amuses me about companies competing with Apple is they always have a product coming out that will kill the one Apple is already shipping. How many iPad, iPod, iPhone killers have there been?

Just once it would be nice to see a company try to compete with something they are actually shipping. As far as I am concerned CurrentC is vaporware.

posted by cjorgensen at 10:17 AM on October 27, 2014 [8 favorites]

Just once it would be nice to see a company try to compete with something they are actually shipping. As far as I am concerned CurrentC is vaporware.

posted by cjorgensen at 10:17 AM on October 27, 2014 [8 favorites]

It's kind of interesting that Google Wallet has been a transaction option in some of these stores for over a year but it's only when Apple Pay launched that the consortium noticed all these NFC-enabled terminals at their retail counters.

posted by ardgedee at 10:18 AM on October 27, 2014 [7 favorites]

posted by ardgedee at 10:18 AM on October 27, 2014 [7 favorites]

If they're billing you after the meal, that could be illegal - there's a reason our currency is marked "legal tender for all debts public and private".

Wrong. I thought that as well, but as long as it's clearly posted they don't have to take cash.

posted by cjorgensen at 10:18 AM on October 27, 2014 [2 favorites]

Wrong. I thought that as well, but as long as it's clearly posted they don't have to take cash.

posted by cjorgensen at 10:18 AM on October 27, 2014 [2 favorites]

You mean the ATM that wasn't to charge me $2.50 to get out $20?

My bank reimburses me for the first $10 of out of network ATM fees, as long as I make 1 direct deposit a month. Get a better bank or take out more than $20 at a time.

posted by T.D. Strange at 10:19 AM on October 27, 2014

My bank reimburses me for the first $10 of out of network ATM fees, as long as I make 1 direct deposit a month. Get a better bank or take out more than $20 at a time.

posted by T.D. Strange at 10:19 AM on October 27, 2014

ACH also provides no consumer level protection against fraud.

The great thing about ACH is that banks will often authorize a transfer, and then four or five days later reverse it because they just noticed that actually the account doesn't exist.

posted by kenko at 10:19 AM on October 27, 2014 [2 favorites]

The great thing about ACH is that banks will often authorize a transfer, and then four or five days later reverse it because they just noticed that actually the account doesn't exist.

posted by kenko at 10:19 AM on October 27, 2014 [2 favorites]

Well, even $100 at a time is a 2.5% usage fee for my own money. All banks in my area are like this. So not really an option to get a better one.

posted by cjorgensen at 10:20 AM on October 27, 2014 [2 favorites]

posted by cjorgensen at 10:20 AM on October 27, 2014 [2 favorites]

NYT (2010): The Merchants That Don’t Take Cash

posted by roomthreeseventeen at 10:20 AM on October 27, 2014 [4 favorites]

posted by roomthreeseventeen at 10:20 AM on October 27, 2014 [4 favorites]

the jam: "Also, the app wants access to your health data. (source)

It's really a shopper's dream. Just... "

And don't forget, the consortium has excellent IT customer service reps waiting to help you should you experience any issue. Just dial 0118 999 881 999 119 725 3 and they'll be able to assist you!

posted by boo_radley at 10:20 AM on October 27, 2014 [9 favorites]

It's really a shopper's dream. Just... "

And don't forget, the consortium has excellent IT customer service reps waiting to help you should you experience any issue. Just dial 0118 999 881 999 119 725 3 and they'll be able to assist you!

posted by boo_radley at 10:20 AM on October 27, 2014 [9 favorites]

Paying for stuff is only one part of the long-term game for Apple Pay:

Apple Eyes New Uses for NFC Beyond iPhone Payments

The Apple representatives have talked to technology providers like HID Global and Cubic, which enable secure access to buildings and transit fare systems, respectively, said people briefed on the discussions. Spokespeople for the companies declined to comment about any discussions with Apple, but executives there discussed how they could integrate their systems with the iPhone.

CurrentC is dead within a year, if the vendors don't cave sooner — maybe they angle for and get a sweeter deal from the merchants — but Apple seems to already be playing a longer game.

posted by a lungful of dragon at 10:21 AM on October 27, 2014

Apple Eyes New Uses for NFC Beyond iPhone Payments

The Apple representatives have talked to technology providers like HID Global and Cubic, which enable secure access to buildings and transit fare systems, respectively, said people briefed on the discussions. Spokespeople for the companies declined to comment about any discussions with Apple, but executives there discussed how they could integrate their systems with the iPhone.

CurrentC is dead within a year, if the vendors don't cave sooner — maybe they angle for and get a sweeter deal from the merchants — but Apple seems to already be playing a longer game.

posted by a lungful of dragon at 10:21 AM on October 27, 2014

Actually I've been in several restaurants that don't accept cash. Card only or go elsewhere.

Is that even legal? And regardless of legality....why? Note that "avoiding having cash on the premises" in this case results in "having credit card data on the premises".

And try paying for something with cash in an Apple store.

Having never been in Apple store, I'm wondering what exactly the issue is here. Do they spit on you or something?

Buying everything I need from the local flea market is looking better every day.

posted by DU at 10:21 AM on October 27, 2014 [1 favorite]

Is that even legal? And regardless of legality....why? Note that "avoiding having cash on the premises" in this case results in "having credit card data on the premises".

And try paying for something with cash in an Apple store.

Having never been in Apple store, I'm wondering what exactly the issue is here. Do they spit on you or something?

Buying everything I need from the local flea market is looking better every day.

posted by DU at 10:21 AM on October 27, 2014 [1 favorite]

Those who cannot remember the CueCat are condemned to repeat it.

posted by Esteemed Offendi at 10:22 AM on October 27, 2014 [35 favorites]

posted by Esteemed Offendi at 10:22 AM on October 27, 2014 [35 favorites]

MCX = Merchant Customer eXchange. They aren't even trying to hide the fact that you're being passed around, merchant to merchant. But hey, at least I get coupons for it!

posted by msbutah at 10:22 AM on October 27, 2014 [6 favorites]

posted by msbutah at 10:22 AM on October 27, 2014 [6 favorites]

Just once it would be nice to see a company try to compete with something they are actually shipping.

To be fair, much of the "wearables" market has been predicated on the idea that Apple is going to release Something in that category. I mean granted that none of the stuff that is out right now is as glorious as the iWatch that Apple will be releasing sometime next year, but, it does happen. There is competition, for sufficiently small values of "compete."

posted by rustcrumb at 10:23 AM on October 27, 2014

To be fair, much of the "wearables" market has been predicated on the idea that Apple is going to release Something in that category. I mean granted that none of the stuff that is out right now is as glorious as the iWatch that Apple will be releasing sometime next year, but, it does happen. There is competition, for sufficiently small values of "compete."

posted by rustcrumb at 10:23 AM on October 27, 2014

Those who cannot remember the CueCat are condemned to repeat it.

So, apologies to those of you who mentioned CueCat earlier, but this is the best CueCat reference thus far in the thread.

posted by aramaic at 10:23 AM on October 27, 2014 [5 favorites]

So, apologies to those of you who mentioned CueCat earlier, but this is the best CueCat reference thus far in the thread.

posted by aramaic at 10:23 AM on October 27, 2014 [5 favorites]

Is that even legal? And regardless of legality....why? Note that "avoiding having cash on the premises" in this case results in "having credit card data on the premises".

The NYT article roomthreeseventeen linked answers this. The TL;DR is it's legal, and it's more of a danger to have cash on premises than credit card data (at least for now).

posted by zombieflanders at 10:24 AM on October 27, 2014

The NYT article roomthreeseventeen linked answers this. The TL;DR is it's legal, and it's more of a danger to have cash on premises than credit card data (at least for now).

posted by zombieflanders at 10:24 AM on October 27, 2014

Technology is supposed to enable disintermediation.

Well, there are several issues that cash intermediaries solve: universal availability of credit, vulnerability to crime or mishap, difficulties for people with loss of motor control or eyesight, and general convenience. All of these are things that have been enabled by technology.

Even ACH, the transaction type being used for CurrentC, is a disintermediation: it's basically a way for banks' computers to talk to each other and say "Give sylvanshine $3000, this is his payroll." The problem is that the retailers are so ignorant about financial software that they think that's all the credit card companies and Google/Apple are doing. It's not. There are fraud detection and protection systems inherent in the intermediaries; refunding and dispute processes; and so on.

An ACH transfer has none of these features. It just happens. If you call your bank and say "Holy shitballs! Someone did an ACH transfer for $2000 out of my account without authorization!" they're going to immediately reverse it (if you've notified them within 60 days of the transfer). Who's left holding the bag? Whoever was supposed to get the money. Unless CVS and Wal-Mart are going to open up an entire legal wing to sue people who are reversing their ACH charges maliciously, they will end up with a pile of liability.

Oh, but what if you don't notice a small ACH transfer until 60 days later? That's all she wrote. Good luck disputing it. (There is no central authority with whom you can dispute the charge.)

posted by sonic meat machine at 10:24 AM on October 27, 2014 [12 favorites]

Well, there are several issues that cash intermediaries solve: universal availability of credit, vulnerability to crime or mishap, difficulties for people with loss of motor control or eyesight, and general convenience. All of these are things that have been enabled by technology.

Even ACH, the transaction type being used for CurrentC, is a disintermediation: it's basically a way for banks' computers to talk to each other and say "Give sylvanshine $3000, this is his payroll." The problem is that the retailers are so ignorant about financial software that they think that's all the credit card companies and Google/Apple are doing. It's not. There are fraud detection and protection systems inherent in the intermediaries; refunding and dispute processes; and so on.

An ACH transfer has none of these features. It just happens. If you call your bank and say "Holy shitballs! Someone did an ACH transfer for $2000 out of my account without authorization!" they're going to immediately reverse it (if you've notified them within 60 days of the transfer). Who's left holding the bag? Whoever was supposed to get the money. Unless CVS and Wal-Mart are going to open up an entire legal wing to sue people who are reversing their ACH charges maliciously, they will end up with a pile of liability.

Oh, but what if you don't notice a small ACH transfer until 60 days later? That's all she wrote. Good luck disputing it. (There is no central authority with whom you can dispute the charge.)

posted by sonic meat machine at 10:24 AM on October 27, 2014 [12 favorites]

Oh, great, now payment services will be just as fragmented as streaming services.

"Sorry, that movie does exist on Netflix but we are unable to process your payment this month because you use ApplePay. Amazon will accept ApplePay but they only have that movie on alternate Thursdays."

posted by bondcliff at 10:25 AM on October 27, 2014 [11 favorites]

"Sorry, that movie does exist on Netflix but we are unable to process your payment this month because you use ApplePay. Amazon will accept ApplePay but they only have that movie on alternate Thursdays."

posted by bondcliff at 10:25 AM on October 27, 2014 [11 favorites]

This is timely, because I was on the phone at 3:00 this morning with Amex because my card had been compromised, no doubt through one of those high-profile data breaches of the past few years--there was a fraudulent charge last night at a 7-11 in Dallas (I live in Massachusetts) and I was surprised they didn't go for more than $30 worth of stuff. The account services rep who handled my claim actually told me the replacement card would be what sounded like a chip and PIN card (maybe I misunderstood, it was 3am after all...)

CurrentC sounds pretty terrible. If I understand what Rite Aid and CVS have done here correctly, it sounds like the ExpressPay RFID thing on my card won't work anymore either, which is annoying. I've been a regular CVS customer but I think I'm going to switch over my prescriptions to Walgreens and start going there instead... it's not much further away than the CVS I usually go to anyway, and I like the Apple Pay experience so far.

posted by Kosh at 10:26 AM on October 27, 2014

CurrentC sounds pretty terrible. If I understand what Rite Aid and CVS have done here correctly, it sounds like the ExpressPay RFID thing on my card won't work anymore either, which is annoying. I've been a regular CVS customer but I think I'm going to switch over my prescriptions to Walgreens and start going there instead... it's not much further away than the CVS I usually go to anyway, and I like the Apple Pay experience so far.

posted by Kosh at 10:26 AM on October 27, 2014

Having never been in Apple store, I'm wondering what exactly the issue is here.

In an Apple store the clerks on the floor can all take your money with these scanners in their iPhones or you can use the App. I paid for an Apple TV using the app and walked in and took it off the shelf and walked out. It took seconds in either case.

Using cash requires you to go the the Genius Bar (and potentially wait in line) to get to the one cash drawer in the place.

posted by cjorgensen at 10:26 AM on October 27, 2014

In an Apple store the clerks on the floor can all take your money with these scanners in their iPhones or you can use the App. I paid for an Apple TV using the app and walked in and took it off the shelf and walked out. It took seconds in either case.

Using cash requires you to go the the Genius Bar (and potentially wait in line) to get to the one cash drawer in the place.

posted by cjorgensen at 10:26 AM on October 27, 2014

That means it CAN be accepted for all debts, it doesn't have to be. If I sell you something on Ebay, I don't have to take cash, I don't think it's really different in person. What it saves you isn't just having cash on premises--it would save you having to send someone to the bank with a ton of cash on a daily basis. It's not the point where it's in the register that it's most dangerous; it's when it's in a package that someone has to physically convey across town somehow. Not to mention that it's a time-consuming task for a trusted employee.

I'm still perfectly happy with my debit card for right now and considering my grocery store will still take personal checks with the right procedure, I'm not seeing them refusing debit cards anytime soon.

I do, however, think that NFC is pretty nifty. I'm hoping more places will get support for the YubiKey with the NFC chip (or something similar) at some point for 2-factor auth so that I can justify the expense, and I'm seriously considering putting a variety of them in my apartment and car for a whole bunch of purposes.

posted by Sequence at 10:26 AM on October 27, 2014

I'm still perfectly happy with my debit card for right now and considering my grocery store will still take personal checks with the right procedure, I'm not seeing them refusing debit cards anytime soon.

I do, however, think that NFC is pretty nifty. I'm hoping more places will get support for the YubiKey with the NFC chip (or something similar) at some point for 2-factor auth so that I can justify the expense, and I'm seriously considering putting a variety of them in my apartment and car for a whole bunch of purposes.

posted by Sequence at 10:26 AM on October 27, 2014

That means it CAN be accepted for all debts, it doesn't have to be.

No, it has to be. But offering to buy something does not therefore incur a debt that you can satisfy this way. It is up to a merchant to decide whether or not to accept your offer, and they can put conditions on it like insisting on payment in advance, via the means of the merchant's choosing.

posted by grouse at 10:30 AM on October 27, 2014 [7 favorites]

No, it has to be. But offering to buy something does not therefore incur a debt that you can satisfy this way. It is up to a merchant to decide whether or not to accept your offer, and they can put conditions on it like insisting on payment in advance, via the means of the merchant's choosing.

posted by grouse at 10:30 AM on October 27, 2014 [7 favorites]

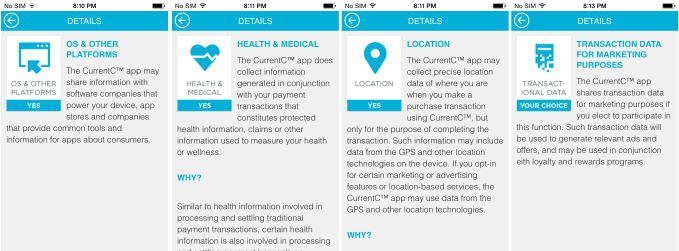

I'm not sure there's a problem with the health information - or at least we can't seem to tell yet. This is the image that is being referenced, and I can't seem to find a full policy. What we can see:

posted by Lemurrhea at 10:31 AM on October 27, 2014 [2 favorites]

{kind=link}

The CurrentC app does collect information generated in conjunction with your payment transactions that constitute protected health information, claims or other information used to measure your health or wellness.and then the image cuts off. At least that part of it reads more like them acknowledging that having a record of your purchases can constitute health info - if I'm buying Lipitor, then they have health info. That's true and not really a change from the present. Can't tell from that image alone whether they share it or exactly what they mean. Anyone have a full policy? Their website is...minimalist.

Why?

Similar to health information involved in processing and settling traditional payment transactions, certain health information is also involved in processing...

posted by Lemurrhea at 10:31 AM on October 27, 2014 [2 favorites]

CurrentC not CurrenC.

It's like they don't even want to be confused with competent branding.

I have a feeling Apple will just block the CurrentC app from the App Store. Seems only fair if they're blocking Apple Pay from their stores.

"Duplicating existing functionality" is the line they'll cite.

posted by ChurchHatesTucker at 10:32 AM on October 27, 2014 [9 favorites]

It's like they don't even want to be confused with competent branding.

I have a feeling Apple will just block the CurrentC app from the App Store. Seems only fair if they're blocking Apple Pay from their stores.

"Duplicating existing functionality" is the line they'll cite.

posted by ChurchHatesTucker at 10:32 AM on October 27, 2014 [9 favorites]

The Register has been calling NFC payment "Pay-by-bonk" and doing po-faced opinion pieces on its perils (there basically are none - the funniest was one that claimed people would be smashing their phones to pieces upon checkout scanners in their enthusiasm to pay for things).

Pay-by-bonk is it - shitloads better than current credit/debit card infrastructure in terms of security and convenience, and CurrenC will be the biggest non-starter since Flooz. Retailers who eschew ApplePay or GoogleWallet - for any reason - are basically telling people who want to make quick purchases to go next door, because this store doesn't like your money. They'll seem to be quaint cranks at best, like the breakfast place that doesn't take credit cards so you never go there even though it's supposed to be good because who the hell has cash at 9:00am on Saturday?

posted by Slap*Happy at 10:34 AM on October 27, 2014 [10 favorites]

Pay-by-bonk is it - shitloads better than current credit/debit card infrastructure in terms of security and convenience, and CurrenC will be the biggest non-starter since Flooz. Retailers who eschew ApplePay or GoogleWallet - for any reason - are basically telling people who want to make quick purchases to go next door, because this store doesn't like your money. They'll seem to be quaint cranks at best, like the breakfast place that doesn't take credit cards so you never go there even though it's supposed to be good because who the hell has cash at 9:00am on Saturday?

posted by Slap*Happy at 10:34 AM on October 27, 2014 [10 favorites]

My neighborhood CVS, located directly across the street from my bank, has a an ATM from my bank. I suspect I'm going to be using it even more so than I do now.

posted by dances with hamsters at 10:34 AM on October 27, 2014

posted by dances with hamsters at 10:34 AM on October 27, 2014

Stolen from Daring Fireball: Can't wait for the mobile payments app from the company that designed this receipt.

posted by cjorgensen at 10:36 AM on October 27, 2014 [22 favorites]

posted by cjorgensen at 10:36 AM on October 27, 2014 [22 favorites]

You know, it's not that big a inconvenience to me to run by the ATM on the way to the store, much less than trying to sort this out.

ATMs in the US are rapidly aging and increasingly prey to increasingly sophisticated skimmers. Trust your bank all you want, but until all banks in the US spend the cash to replace their armada of decrepit ATMs, I don't trust any ATM.

Doesn't mean I don't use them, because they are, let's face it, convenient -- and 9 times out of 10, banks find ways to force you to use them rather than come in to do in-branch transactions. Doesn't mean I don't cringe every time I have to use one.

posted by blucevalo at 10:37 AM on October 27, 2014 [3 favorites]

ATMs in the US are rapidly aging and increasingly prey to increasingly sophisticated skimmers. Trust your bank all you want, but until all banks in the US spend the cash to replace their armada of decrepit ATMs, I don't trust any ATM.

Doesn't mean I don't use them, because they are, let's face it, convenient -- and 9 times out of 10, banks find ways to force you to use them rather than come in to do in-branch transactions. Doesn't mean I don't cringe every time I have to use one.

posted by blucevalo at 10:37 AM on October 27, 2014 [3 favorites]

The Apple representatives have talked to technology providers like HID Global and Cubic, which enable secure access to buildings and transit fare systems, respectively, said people briefed on the discussions. Spokespeople for the companies declined to comment about any discussions with Apple, but executives there discussed how they could integrate their systems with the iPhone.

So that's creepy.

At work, there's already pressure to have an iPhone - one of the systems we use has a validation process which is much quicker with the iPhone than without.

I have always been "well, a drawback of the iPhone is that you are apparently completely trackable and that's very difficult to turn off, whereas there's more workarounds for old-fashioned phones"....Apple, apparently sensing how creepy and surveillance-y most of their products are, is I guess just going full on into security/surveillance industry. Next up, maybe they'll run the prisons. Or the cops, that would probably be the quickest route.

posted by Frowner at 10:37 AM on October 27, 2014 [4 favorites]

Putting aside the shitty behavior of CVS, etc, perhaps most alarming about this is the QR codes. Seriously?

I mean, I'm not one to put much stock in fear-mongering stories about people photographing your credit card when you take it out of your wallet. However, QR codes are basically designed to be machine-readable at a distance. That seems like a rather easy target for capture and fraud.

posted by tocts at 10:37 AM on October 27, 2014 [4 favorites]

I mean, I'm not one to put much stock in fear-mongering stories about people photographing your credit card when you take it out of your wallet. However, QR codes are basically designed to be machine-readable at a distance. That seems like a rather easy target for capture and fraud.

posted by tocts at 10:37 AM on October 27, 2014 [4 favorites]

Most ATMs are also still running Windows XP.

posted by cjorgensen at 10:38 AM on October 27, 2014 [2 favorites]

posted by cjorgensen at 10:38 AM on October 27, 2014 [2 favorites]

NYT (2010): The Merchants That Don’t Take Cash

There are quite a few restaurants that I go to that still will only take cash.

posted by octothorpe at 10:38 AM on October 27, 2014 [2 favorites]

There are quite a few restaurants that I go to that still will only take cash.

posted by octothorpe at 10:38 AM on October 27, 2014 [2 favorites]

No, it has to be. But offering to buy something does not therefore incur a debt that you can satisfy this way. It is up to a merchant to decide whether or not to accept your offer, and they can put conditions on it like insisting on payment in advance, via the means of the merchant's choosing.

Seems like a restaurant serving you a meal with the expectation of payment afterwards has created a debt. And we all know cash is "legal tender for all debts." But I'm not sure if the restaurant still gets away with it because a) it posted a no cash policy or b) legally it's not a debt even though it kinda seems that way.

posted by mullacc at 10:39 AM on October 27, 2014

Seems like a restaurant serving you a meal with the expectation of payment afterwards has created a debt. And we all know cash is "legal tender for all debts." But I'm not sure if the restaurant still gets away with it because a) it posted a no cash policy or b) legally it's not a debt even though it kinda seems that way.

posted by mullacc at 10:39 AM on October 27, 2014

Right place, wrong time. In 1999, I worked for a place that made an RFID reader in the form factor of a mouse pad. NFC and RFID are pretty much the same technology, although RFID tags are allegedly static, but we were looking at various chips that had read/write capability and a small amount of processing power.

The notion was simple, the RFID reader has a unique ID, your credit card has a unique ID and you have a PIN. Then if you're performing an online transaction, the PIN and reader ID authorize the transaction and the RFID ID is used to look up your payment information somewhere not on your computer which then authorizes payment to the site.

It failed as a company because at the time no credit card issuer/bank wanted to invest in helping make the readers ubiquitous nor did they want to pay for the extra cost of a having the tag in their credit cards.

Then there was the challenge that if you're good at making antennae, you can make some pretty awesome RFID skimmers. The mousepad form factor would give a good, solid read in something like 10 inches if the tag was in the right orientation. The problem is that the protocols are very simple - there's a little hand shaking when the chip in the tag powers up and ultimately all it does is say "My ID is xxxxxxxx". In reality, there has to be something more complicated like the ID asking "who goes there, friend or foe?" and not giving up an ID in clear data, but that drives the cost up.

So the response is, go ahead and broadcast your ID, but we'll use the ID in reader which we can keep more private AND the tag ID and we'll take a PIN to as well.

In reality, the whole thing was a solution in search of a problem. Mobil was trying to get in there with Speedpass at the gas pump using a TIRIS tag on a key fob.

Now you have NFC in your phone which solves the ubiquity to a degree and creates the opportunity better security.

I honestly don't expect this to be done right by anyone, although I think the credit card companies are starting to come around to accepting the inevitability of the end of credit cards, but the thing is that what they replace it with will probably be no better than the typical security through obscurity approach which is cheap and makes it cheap to counterfeit.

posted by plinth at 10:39 AM on October 27, 2014 [7 favorites]

The notion was simple, the RFID reader has a unique ID, your credit card has a unique ID and you have a PIN. Then if you're performing an online transaction, the PIN and reader ID authorize the transaction and the RFID ID is used to look up your payment information somewhere not on your computer which then authorizes payment to the site.

It failed as a company because at the time no credit card issuer/bank wanted to invest in helping make the readers ubiquitous nor did they want to pay for the extra cost of a having the tag in their credit cards.

Then there was the challenge that if you're good at making antennae, you can make some pretty awesome RFID skimmers. The mousepad form factor would give a good, solid read in something like 10 inches if the tag was in the right orientation. The problem is that the protocols are very simple - there's a little hand shaking when the chip in the tag powers up and ultimately all it does is say "My ID is xxxxxxxx". In reality, there has to be something more complicated like the ID asking "who goes there, friend or foe?" and not giving up an ID in clear data, but that drives the cost up.

So the response is, go ahead and broadcast your ID, but we'll use the ID in reader which we can keep more private AND the tag ID and we'll take a PIN to as well.

In reality, the whole thing was a solution in search of a problem. Mobil was trying to get in there with Speedpass at the gas pump using a TIRIS tag on a key fob.

Now you have NFC in your phone which solves the ubiquity to a degree and creates the opportunity better security.

I honestly don't expect this to be done right by anyone, although I think the credit card companies are starting to come around to accepting the inevitability of the end of credit cards, but the thing is that what they replace it with will probably be no better than the typical security through obscurity approach which is cheap and makes it cheap to counterfeit.

posted by plinth at 10:39 AM on October 27, 2014 [7 favorites]

So I guess the CurrentC app is in the App Store. The reviews are pretty entertaining.

posted by R. Mutt at 10:40 AM on October 27, 2014

posted by R. Mutt at 10:40 AM on October 27, 2014

When credit cards first started becoming a thing, was there this kind of fragmentation? Some stores took Visa and only Visa, others took Mastercard and only Mastercard, etc? Were there noncompetes involved in being able to take a particular brand of card?

I genuinely don't know the answer to that, but at least by now, that's mostly worked itself out, with most places taking a variety of cards (still annoys me that Costco only takes AmEx though). I don't understand why these companies would look at the success and ubiquity of the credit card model and go "Nah, that's not for us."

posted by kafziel at 10:41 AM on October 27, 2014

I genuinely don't know the answer to that, but at least by now, that's mostly worked itself out, with most places taking a variety of cards (still annoys me that Costco only takes AmEx though). I don't understand why these companies would look at the success and ubiquity of the credit card model and go "Nah, that's not for us."

posted by kafziel at 10:41 AM on October 27, 2014

businesses that don't take cash

Read all you want.

posted by cjorgensen at 10:42 AM on October 27, 2014

Read all you want.

posted by cjorgensen at 10:42 AM on October 27, 2014

Oh, but what if you don't notice a small ACH transfer until 60 days later? That's all she wrote.

And if it's a business account? You get two days, not two months, before the debit is irrevocable. The only safe practice for a small business is 1. check your transactions daily, and 2. don't use checks.

posted by nicwolff at 10:43 AM on October 27, 2014 [1 favorite]

And if it's a business account? You get two days, not two months, before the debit is irrevocable. The only safe practice for a small business is 1. check your transactions daily, and 2. don't use checks.

posted by nicwolff at 10:43 AM on October 27, 2014 [1 favorite]

So I saw this commercial in which some pro football player was attempting to pay for something with his phone while catching tossed balls... I can't remember which service he was using. Seems it would have been easier to swipe a finger print using Apple Pay.

posted by Gungho at 10:45 AM on October 27, 2014

posted by Gungho at 10:45 AM on October 27, 2014

I suppose both Apple and Google could claim they're entitled to their usual 30% cut of all purchases made through th application.

posted by Fruny at 10:45 AM on October 27, 2014 [8 favorites]

posted by Fruny at 10:45 AM on October 27, 2014 [8 favorites]

I recently moved to Denmark, and learned about the system here : Dankort..

Seems like an interesting solution, but it may work best in a smallish country. And as a recent newcomer, it's a pain because I can't get one immediately. .

posted by nat at 10:45 AM on October 27, 2014

Seems like an interesting solution, but it may work best in a smallish country. And as a recent newcomer, it's a pain because I can't get one immediately. .

posted by nat at 10:45 AM on October 27, 2014

ATMs in the US are rapidly aging and increasingly prey to increasingly sophisticated skimmers.

Unless you go all cash and only withdraw at in-person visits, you have to trust your banking info to someone, at some point in the electronic transaction chain. At least your bank or credit card company should have developed fraud reimbursement procedures, unfortunately breaches seem to be a transaction cost of modern banking, and as plinth said, it doesn't look like that's changing

posted by T.D. Strange at 10:46 AM on October 27, 2014 [1 favorite]

Unless you go all cash and only withdraw at in-person visits, you have to trust your banking info to someone, at some point in the electronic transaction chain. At least your bank or credit card company should have developed fraud reimbursement procedures, unfortunately breaches seem to be a transaction cost of modern banking, and as plinth said, it doesn't look like that's changing

posted by T.D. Strange at 10:46 AM on October 27, 2014 [1 favorite]

So I guess the CurrentC app is in the App Store. The reviews are pretty entertaining.

CurrentC

9 five star reviews, 0 four, 1 three, 1 two, and 1,217 one star reviews.

posted by cjorgensen at 10:46 AM on October 27, 2014 [18 favorites]

CurrentC

9 five star reviews, 0 four, 1 three, 1 two, and 1,217 one star reviews.

posted by cjorgensen at 10:46 AM on October 27, 2014 [18 favorites]

I'd like to register my prediction that muggings will now include thumb amputations.

posted by sonascope at 10:46 AM on October 27, 2014 [3 favorites]

posted by sonascope at 10:46 AM on October 27, 2014 [3 favorites]

I honestly don't expect this to be done right by anyone

Aren't NFC payments pretty ubiquitous in East Asia and parts of Europe?

When credit cards first started becoming a thing, was there this kind of fragmentation?

1969 called, they were wondering if Metafilter accepts Diners Club. And well, my Target CC only works at Target, so it's not like this fragmentation is totally licked.

posted by FJT at 10:47 AM on October 27, 2014 [2 favorites]

Aren't NFC payments pretty ubiquitous in East Asia and parts of Europe?

When credit cards first started becoming a thing, was there this kind of fragmentation?

1969 called, they were wondering if Metafilter accepts Diners Club. And well, my Target CC only works at Target, so it's not like this fragmentation is totally licked.

posted by FJT at 10:47 AM on October 27, 2014 [2 favorites]

I was a little sad to CVS included in this consortium. I was all full of good will toward them for dropping tobacco products, and now they go and pull something like this. I also shop at Target some. I wonder if the Kohls next to them will take Apple Pay.

posted by TedW at 10:47 AM on October 27, 2014 [5 favorites]

posted by TedW at 10:47 AM on October 27, 2014 [5 favorites]

I suppose both Apple and Google could claim they're entitled to their usual 30% cut of all purchases made through the application.

This is actually interesting. Again, from Daring Fireball: Apple Said to Negotiate Deep Payments Discounts From Big Banks

Basically Apple is taking a bigger cut than normal from the banks because Apple is assuming the fraud risk. Win/win for Apple.

posted by cjorgensen at 10:49 AM on October 27, 2014

This is actually interesting. Again, from Daring Fireball: Apple Said to Negotiate Deep Payments Discounts From Big Banks

Basically Apple is taking a bigger cut than normal from the banks because Apple is assuming the fraud risk. Win/win for Apple.

posted by cjorgensen at 10:49 AM on October 27, 2014

This is the sort of thing that actually makes me care about distributed cryptocurrencies. I don't much care for anarcholibertarianism, but it beats panopticon capitalism (except where it's equivalent).

All the cryptocurrencies I know of operate by making all transactions a public record. Everyone in the world knows and agrees that wallet 123456789 paid wallet 987654321 0.24 crypto-coins. The only thing private about it is that we don't know who owns those wallets. Which seems ripe for big data type analysis, or merchant collusion, or information leaked from hacks, or whatever.

posted by aubilenon at 10:51 AM on October 27, 2014 [6 favorites]

All the cryptocurrencies I know of operate by making all transactions a public record. Everyone in the world knows and agrees that wallet 123456789 paid wallet 987654321 0.24 crypto-coins. The only thing private about it is that we don't know who owns those wallets. Which seems ripe for big data type analysis, or merchant collusion, or information leaked from hacks, or whatever.

posted by aubilenon at 10:51 AM on October 27, 2014 [6 favorites]

9 five star reviews, 0 four, 1 three, 1 two, and 1,217 one star reviews.

Unfortunately, the App Store doesn't allow zero-star ratings.

posted by Thorzdad at 10:51 AM on October 27, 2014 [1 favorite]

Unfortunately, the App Store doesn't allow zero-star ratings.

posted by Thorzdad at 10:51 AM on October 27, 2014 [1 favorite]

sonascope: I'd like to register my prediction that muggings will now include thumb amputations.

Nope. TouchID only works with living fingers: "Apple is not the first company to design a robust fingerprint sensor that is able to "avoid dead fingers"

posted by blob at 10:53 AM on October 27, 2014 [7 favorites]

Nope. TouchID only works with living fingers: "Apple is not the first company to design a robust fingerprint sensor that is able to "avoid dead fingers"

posted by blob at 10:53 AM on October 27, 2014 [7 favorites]

I also shop at Target some. I wonder if the Kohls next to them will take Apple Pay.

Kohl's is a member of MCX, so presumably not. What's odd about Target is that their iOS app supports Apple Pay. It's unclear how this is not in violation of the exclusivity agreement.

posted by entropicamericana at 10:53 AM on October 27, 2014 [1 favorite]

Kohl's is a member of MCX, so presumably not. What's odd about Target is that their iOS app supports Apple Pay. It's unclear how this is not in violation of the exclusivity agreement.

posted by entropicamericana at 10:53 AM on October 27, 2014 [1 favorite]

I'd like to register my prediction that muggings will now include thumb amputations.

touchID and dead fingers

Also, my phone isn't linked to my thumb. You're gonna have to take all 10 to be sure (and my nipples).

posted by cjorgensen at 10:54 AM on October 27, 2014 [3 favorites]

touchID and dead fingers

Also, my phone isn't linked to my thumb. You're gonna have to take all 10 to be sure (and my nipples).

posted by cjorgensen at 10:54 AM on October 27, 2014 [3 favorites]

INSERT FINGER

CASH WILL DISPENSE AUTOMATICALLY

AVOID DEAD FINGERS FOR HIGH SCORE

posted by griphus at 10:54 AM on October 27, 2014 [13 favorites]

CASH WILL DISPENSE AUTOMATICALLY

AVOID DEAD FINGERS FOR HIGH SCORE

posted by griphus at 10:54 AM on October 27, 2014 [13 favorites]

I sometimes wonder if there is something inherent in the nature of a business person that makes them unusually amenable to cutting off their nose in order to spite their face.

posted by aramaic at 10:55 AM on October 27, 2014 [4 favorites]

posted by aramaic at 10:55 AM on October 27, 2014 [4 favorites]

I use cash at just about every national or regional chain we shop at and that's the way it's been for a couple years. I do used my debit card at the grocery store and to fill on gas - I suppose that I'll get burned by that one of these days. If Amazon gets cracked then I'm in trouble.

posted by Ber at 10:56 AM on October 27, 2014

posted by Ber at 10:56 AM on October 27, 2014

Read all you want.

My (possibly out of date) understanding: Businesses don't have to accept cash up front. So, if someone offers to buy your lemonade with cash, you could refuse. However, if you serve lemonade to someone and when the bill comes they offer to pay in cash, refusing that cash is canceling the debt.

Nothing in the above links seem to contradict that.

posted by ChurchHatesTucker at 10:56 AM on October 27, 2014

My (possibly out of date) understanding: Businesses don't have to accept cash up front. So, if someone offers to buy your lemonade with cash, you could refuse. However, if you serve lemonade to someone and when the bill comes they offer to pay in cash, refusing that cash is canceling the debt.

Nothing in the above links seem to contradict that.

posted by ChurchHatesTucker at 10:56 AM on October 27, 2014

Well, now I see that Kohls is part of the evil MCX, so I guess I can't use Apple Pay there or Target. But I also notice that at least one retailer (Meijer) is part of both groups, so perhaps they aren't as mutually exclusive as some are saying.

posted by TedW at 10:59 AM on October 27, 2014

posted by TedW at 10:59 AM on October 27, 2014

I sometimes wonder if there is something inherent in the nature of a business person that makes them unusually amenable to cutting off their nose in order to spite their face.

The enmity is personal, the money isn't.

posted by ChurchHatesTucker at 11:00 AM on October 27, 2014

The enmity is personal, the money isn't.

posted by ChurchHatesTucker at 11:00 AM on October 27, 2014

My credit card has been compromised four times in the last 2 years. Target (which completes the irony of them forgoing a secure technology on favor of embracing an insecure one), Lacie, Home Depot and one other place. It's literally happened enough that I've forgotten which places have done it. I am moving away from credit cards for this reason (and others). I won't shop in a Target again unless it's with cash. I don't think I've been back there since. Same with Lacie. I canceled my outstanding orders with them and won't buy from them again. In the Lacie case it was also my username/password for their site.

I'm down to one credit card. I would love to get rid of that. My previous plan was to open a checking account. Use the debit card on it, keeping only what I needed in there. So the idea of a newer, more secure way to pay, appeals to me.

posted by cjorgensen at 11:01 AM on October 27, 2014

I'm down to one credit card. I would love to get rid of that. My previous plan was to open a checking account. Use the debit card on it, keeping only what I needed in there. So the idea of a newer, more secure way to pay, appeals to me.

posted by cjorgensen at 11:01 AM on October 27, 2014

I have always been "well, a drawback of the iPhone is that you are apparently completely trackable and that's very difficult to turn off, whereas there's more workarounds for old-fashioned phones"... Apple, apparently sensing how creepy and surveillance-y most of their products are, is I guess just going full on into security/surveillance industry.

As described, Apple doesn't get to know anything about the details of the transaction between end user and vendor.

My guess is that using NFC for building access would work the same way, where the token exchange starts and ends between the end user and the building's maintenance system (which presumably Apple has no interest in, for the same reason it does not track purchase sessions).

But people are already trackable by means of other technologies, such as making a purchase with a plain credit card, or using a popular web-based email system that scans purchase-related and other personal emails for targeted advertising.

Privacy laws are probably a weak point worth focusing on, generally.

posted by a lungful of dragon at 11:01 AM on October 27, 2014 [1 favorite]

As described, Apple doesn't get to know anything about the details of the transaction between end user and vendor.

My guess is that using NFC for building access would work the same way, where the token exchange starts and ends between the end user and the building's maintenance system (which presumably Apple has no interest in, for the same reason it does not track purchase sessions).

But people are already trackable by means of other technologies, such as making a purchase with a plain credit card, or using a popular web-based email system that scans purchase-related and other personal emails for targeted advertising.

Privacy laws are probably a weak point worth focusing on, generally.

posted by a lungful of dragon at 11:01 AM on October 27, 2014 [1 favorite]

Uh, so I never thought I would type this, but I LIKE my credit card!

It has fraud protection, so I'm not on the hook for lax security at any end of the chain of purchase. It's convenient, small, and accepted everywhere. I also don't have to have a charged phone for it to operate. I get rewards points, and just pay it off every statement anyway. I'm basically getting free money in the form of points instead of absolutely nothing for using cash or my debit card.

The cost for this is largely passed on to retailers and people who maintain a revolving balance of debt, but neither one of those things describes me, so strangely I'm actually on the losing side of the equation if credit cards start to go extinct. But, looking at the MCX documentation, I don't see that happening any time soon.

posted by codacorolla at 11:01 AM on October 27, 2014 [26 favorites]

It has fraud protection, so I'm not on the hook for lax security at any end of the chain of purchase. It's convenient, small, and accepted everywhere. I also don't have to have a charged phone for it to operate. I get rewards points, and just pay it off every statement anyway. I'm basically getting free money in the form of points instead of absolutely nothing for using cash or my debit card.

The cost for this is largely passed on to retailers and people who maintain a revolving balance of debt, but neither one of those things describes me, so strangely I'm actually on the losing side of the equation if credit cards start to go extinct. But, looking at the MCX documentation, I don't see that happening any time soon.

posted by codacorolla at 11:01 AM on October 27, 2014 [26 favorites]

9 five star reviews, 0 four, 1 three, 1 two, and 1,217 one star reviews.

At least two of those "five star" reviews are 100% sarcasm. "Please track all my movements on your store wifi and sell all my data to junk mail companies too!"

posted by dnash at 11:02 AM on October 27, 2014 [2 favorites]

At least two of those "five star" reviews are 100% sarcasm. "Please track all my movements on your store wifi and sell all my data to junk mail companies too!"

posted by dnash at 11:02 AM on October 27, 2014 [2 favorites]

Is there where I just in to say I've been using "Tap to Pay" with my debit+credit cards for years in Canada? ApplePay is the same system, just differently branded.

posted by blue_beetle at 11:03 AM on October 27, 2014 [5 favorites]

posted by blue_beetle at 11:03 AM on October 27, 2014 [5 favorites]

CVS is already the absolute worst on privacy protection.

I'm never showing them my card again (I have to go there because that's my mandatory prescription pharmacy--thanks insurance!). Also I can vouch for those horrendous receipts; I've gotten them myself. They use more (thermal) paper in the receipt than the bag for most of my scrips.

posted by immlass at 11:06 AM on October 27, 2014

I'm never showing them my card again (I have to go there because that's my mandatory prescription pharmacy--thanks insurance!). Also I can vouch for those horrendous receipts; I've gotten them myself. They use more (thermal) paper in the receipt than the bag for most of my scrips.

posted by immlass at 11:06 AM on October 27, 2014

Is there where I just in to say I've been using "Tap to Pay" with my debit+credit cards for years in Canada? ApplePay is the same system, just differently branded.

No. It's not. Your Tap to Pay still sends the PAN to the pinpad which can then be hijacked or just stored by the merchant for later breaches.

Apple Pay converts the PAN to a Device Account Number which is then used to assign a unique signature to each transaction.

posted by Talez at 11:07 AM on October 27, 2014 [10 favorites]

No. It's not. Your Tap to Pay still sends the PAN to the pinpad which can then be hijacked or just stored by the merchant for later breaches.

Apple Pay converts the PAN to a Device Account Number which is then used to assign a unique signature to each transaction.

posted by Talez at 11:07 AM on October 27, 2014 [10 favorites]

The cloud is safe and secure for your money and biometric data linked to said money.

Just don't put nekkid selfies up there and expect them to remain secure. That's crazy talk.

posted by Pirate-Bartender-Zombie-Monkey at 11:09 AM on October 27, 2014 [10 favorites]

Just don't put nekkid selfies up there and expect them to remain secure. That's crazy talk.

posted by Pirate-Bartender-Zombie-Monkey at 11:09 AM on October 27, 2014 [10 favorites]

So, is ACH actually any scarier than a debit card transaction? AFAIK, the fraud protection mechanisms in the debit system are pretty weak.

Really, I'd love for us to figure out a way to do open payments correctly (and kill Visa's stranglehold on payment processing in the process). It's staggering that the only good replacement for paper checks is still PayPal.

Also, unless Apple want to evolve into a payment processor, Apple Pay isn't going to be a long-term solution for anything. It's a weirdly ambitious business venture for Apple, and it's not at all clear what their endgame is -- do they expect to convert everybody to iOS? Open the platform? Only exist as a secondary payment system?

Apple's strength has always been in the focus of its product offerings, which lately have also been quite conservative as well (not necessarily a bad thing -- Apple don't launch half-baked products). "Try everything and see what sticks" has never worked well for Apple -- that's what Amazon and Google do, and it's particularly perplexing that Apple are seemingly willing to spend a substantial amount of political capital on launching a product, where many other extremely competent players have failed spectacularly due to industry and consumer opposition.

I can be a pretty harsh critic of Apple, but I like the payment processing cartels even less. Apple Pay adds value to the iPhone portfolio, but probably isn't going to attract many new people to the platform. Why not work with Google, Amazon, et al, and actually come up with an industry standard that consumers and businesses can all get on board with?

posted by schmod at 11:10 AM on October 27, 2014

Really, I'd love for us to figure out a way to do open payments correctly (and kill Visa's stranglehold on payment processing in the process). It's staggering that the only good replacement for paper checks is still PayPal.

Also, unless Apple want to evolve into a payment processor, Apple Pay isn't going to be a long-term solution for anything. It's a weirdly ambitious business venture for Apple, and it's not at all clear what their endgame is -- do they expect to convert everybody to iOS? Open the platform? Only exist as a secondary payment system?

Apple's strength has always been in the focus of its product offerings, which lately have also been quite conservative as well (not necessarily a bad thing -- Apple don't launch half-baked products). "Try everything and see what sticks" has never worked well for Apple -- that's what Amazon and Google do, and it's particularly perplexing that Apple are seemingly willing to spend a substantial amount of political capital on launching a product, where many other extremely competent players have failed spectacularly due to industry and consumer opposition.

I can be a pretty harsh critic of Apple, but I like the payment processing cartels even less. Apple Pay adds value to the iPhone portfolio, but probably isn't going to attract many new people to the platform. Why not work with Google, Amazon, et al, and actually come up with an industry standard that consumers and businesses can all get on board with?

posted by schmod at 11:10 AM on October 27, 2014

Was this a result of some sort of challenge to make BitCoin actually look good by comparison?

Among other things. After much debate on what to link to, I decided to take a short cut.

posted by infini at 11:10 AM on October 27, 2014 [1 favorite]

Among other things. After much debate on what to link to, I decided to take a short cut.

posted by infini at 11:10 AM on October 27, 2014 [1 favorite]

I like my credit cards, too. That's why I like to use Google Wallet. Same zero fraud liability and no risk of a merchant breach giving my actual card number to crooks.

I also have a Google Wallet card for those places that don't do NFC, but my Wallet balance is usually around $3 so that's less helpful than it might seem. Of course, the fraud protection on my wallet balance isn't that great compared to credit, so better not to have a big wallet balance anyway. I mainly end up using it to avoid my bank's (small) foreign ATM transaction fee.

posted by wierdo at 11:11 AM on October 27, 2014 [1 favorite]

I also have a Google Wallet card for those places that don't do NFC, but my Wallet balance is usually around $3 so that's less helpful than it might seem. Of course, the fraud protection on my wallet balance isn't that great compared to credit, so better not to have a big wallet balance anyway. I mainly end up using it to avoid my bank's (small) foreign ATM transaction fee.

posted by wierdo at 11:11 AM on October 27, 2014 [1 favorite]

If you had read the links, you would know that the biometric information from TouchID never leaves your device.

posted by entropicamericana at 11:12 AM on October 27, 2014 [4 favorites]

posted by entropicamericana at 11:12 AM on October 27, 2014 [4 favorites]

Why not work with Google, Amazon, et al, and actually come up with an industry standard that consumers and businesses can all get on board with?

Apple Pay is an adaption of the EMVCo tokenization and NFC standards. Google Wallet uses the NFC standard but I believe it replaces the PAN (in theory) with a prepaid Mastercard number for that transaction as a hacked up version of tokenization.

posted by Talez at 11:13 AM on October 27, 2014 [2 favorites]

Apple Pay is an adaption of the EMVCo tokenization and NFC standards. Google Wallet uses the NFC standard but I believe it replaces the PAN (in theory) with a prepaid Mastercard number for that transaction as a hacked up version of tokenization.

posted by Talez at 11:13 AM on October 27, 2014 [2 favorites]

schmod, my understanding is that, like Google Wallet, Apple Pay works on any standard NFC reader. It's surprisingly non-proprietary, at least by Apple's usual standard.

posted by wierdo at 11:13 AM on October 27, 2014 [1 favorite]

posted by wierdo at 11:13 AM on October 27, 2014 [1 favorite]

9 five star reviews, 0 four, 1 three, 1 two, and 1,217 one star reviews.

Given the uninformed panic over the Facebook Chat rollout -- and preponderance of user reviews that hadn't actually used the app, I wouldn't read too much into this.*

I mean, it's a bad idea. But the court of public opinion is dumb as dirt when it comes to this stuff.

Facebook are creepy assholes, and people should be upset about that, but they didn't actually change anything by launching a separate chat app.

posted by schmod at 11:15 AM on October 27, 2014 [1 favorite]

Given the uninformed panic over the Facebook Chat rollout -- and preponderance of user reviews that hadn't actually used the app, I wouldn't read too much into this.*

I mean, it's a bad idea. But the court of public opinion is dumb as dirt when it comes to this stuff.

Facebook are creepy assholes, and people should be upset about that, but they didn't actually change anything by launching a separate chat app.

posted by schmod at 11:15 AM on October 27, 2014 [1 favorite]

Apple Pay is an adaption of the EMVCo tokenization and NFC standards.

Does this mean a retailer who converts to terminals that take EMV cards will have no choice but to take Apple Pay?

Also, what is PAN?

posted by mullacc at 11:15 AM on October 27, 2014

Does this mean a retailer who converts to terminals that take EMV cards will have no choice but to take Apple Pay?

Also, what is PAN?

posted by mullacc at 11:15 AM on October 27, 2014

A few months ago, Verizon force-installed an app on my phone called ISIS Mobile Wallet.

This raised so many questions. Why was this installed without my consent? Why do Verizon think that they can compete in this space -- are they still blindly following the Bell Labs Manual For World Domination? Why can't I uninstall it? Why did they name it after a terrorist cell? How quickly can I install CyanogenMod on my new phone?

posted by schmod at 11:17 AM on October 27, 2014 [4 favorites]

This raised so many questions. Why was this installed without my consent? Why do Verizon think that they can compete in this space -- are they still blindly following the Bell Labs Manual For World Domination? Why can't I uninstall it? Why did they name it after a terrorist cell? How quickly can I install CyanogenMod on my new phone?

posted by schmod at 11:17 AM on October 27, 2014 [4 favorites]

Still not really understanding how ApplePay can dominate the market without licensing to third parties. So it continues to sound like a dead end, to me.

posted by lodurr at 11:18 AM on October 27, 2014 [1 favorite]

posted by lodurr at 11:18 AM on October 27, 2014 [1 favorite]

I like my Google Wallet. Seems they use a proxy with the merchant and my credit card info is buried in PlayStore... CVS was one of the better places in terms of integration.

posted by mikelieman at 11:19 AM on October 27, 2014

posted by mikelieman at 11:19 AM on October 27, 2014

Does this mean a retailer who converts to terminals that take EMV cards will have no choice but to take Apple Pay?

No. Apple Pay uses NFC. If the retailer turns off NFC they can still accept Chip and Pin cards without issue.

Also, what is PAN?

PAN is Primary Account Number, the credit card number effectively.

Still not really understanding how ApplePay can dominate the market without licensing to third parties. So it continues to sound like a dead end, to me.

It doesn't have to. It's an implementation of an existing standard. It's like wondering how Apple can dominate music without licensing AAC to other parties. It's not only illogical but literally impossible seeing as they don't own the standard.

posted by Talez at 11:20 AM on October 27, 2014 [5 favorites]

No. Apple Pay uses NFC. If the retailer turns off NFC they can still accept Chip and Pin cards without issue.

Also, what is PAN?

PAN is Primary Account Number, the credit card number effectively.

Still not really understanding how ApplePay can dominate the market without licensing to third parties. So it continues to sound like a dead end, to me.

It doesn't have to. It's an implementation of an existing standard. It's like wondering how Apple can dominate music without licensing AAC to other parties. It's not only illogical but literally impossible seeing as they don't own the standard.

posted by Talez at 11:20 AM on October 27, 2014 [5 favorites]