where does money come from?

June 26, 2019 1:02 PM Subscribe

Neoliberalism has tricked us into believing a fairytale about where money comes from (Mary Mellor, The Conversation).

How did we end up in this neoliberal, austerity ridden hell world ? The economic arguments adopted by Britain and the US in the 1980s led to vastly increased inequality – and gave the false impression that this outcome was not only inevitable, but good.

THE IMF CONFIRMS THAT 'TRICKLE-DOWN' ECONOMICS IS, INDEED, A JOKE

posted by The Whelk at 1:30 PM on June 26, 2019 [17 favorites]

THE IMF CONFIRMS THAT 'TRICKLE-DOWN' ECONOMICS IS, INDEED, A JOKE

posted by The Whelk at 1:30 PM on June 26, 2019 [17 favorites]

From the linked article: Unlike sovereign money, which was created and spent directly into circulation, modern money is largely borrowed into circulation through the banking system. This process shelters behind another myth, that banks merely act as a link between savers and borrowers. In fact, banks create money. And it is only in the last decade that this powerful myth has been finally put to rest by banking and monetary authorities.

It is now acknowledged by monetary authorities such as the IMF, the US Federal Reserve and the Bank of England, that banks are creating new money when they make loans. They don’t lend the money of other account holders to those who want to borrow.

Bank loans consist of money conjured out of thin air, whereby new money is credited to the borrowers account with the agreement that the amount will eventually be repaid with interest.

Neat! TIL.

posted by bagel at 1:37 PM on June 26, 2019 [10 favorites]

It is now acknowledged by monetary authorities such as the IMF, the US Federal Reserve and the Bank of England, that banks are creating new money when they make loans. They don’t lend the money of other account holders to those who want to borrow.

Bank loans consist of money conjured out of thin air, whereby new money is credited to the borrowers account with the agreement that the amount will eventually be repaid with interest.

Neat! TIL.

posted by bagel at 1:37 PM on June 26, 2019 [10 favorites]

I've been saying for a while now that Modern Monetary Theory squares with classic, Keynesian economics just dandy.

Imagine your regular economy, as you may have learned in rudimentary economics. Now add one giant, Scrooge McDuck money vault, seized by or bequeathed to the government.

They could spend it all right away, but that would cause inflation as money was proved to be more plentiful, and the government's demand raised prices. So the government would still have incentive to spend in a measured way.

They could stop taxing, as they've got all the money they need, but that would allow people and companies to accumulate wealth and enforce castes and aristocracies. Additionally, without removing money from the economy, again, we'd see inflation. So the government would still have incentive to tax in a measured way.

They could stop issuing bonds, as again, they don't need the investment, but people like government bonds. They like having a minimum guaranteed return backed by the security of the government.

How much money is in the vault? Well at one point, Uncle Scrooge knew to the penny. But the government seized it and just put it in a black box labeled "money." And as time passed, it became unnecessary to even believe this box existed. As long as people have faith in the US government and demand for the US dollar, this all works, whether the box is a real vault or electronic ledgers.

posted by explosion at 1:50 PM on June 26, 2019 [9 favorites]

Imagine your regular economy, as you may have learned in rudimentary economics. Now add one giant, Scrooge McDuck money vault, seized by or bequeathed to the government.

They could spend it all right away, but that would cause inflation as money was proved to be more plentiful, and the government's demand raised prices. So the government would still have incentive to spend in a measured way.

They could stop taxing, as they've got all the money they need, but that would allow people and companies to accumulate wealth and enforce castes and aristocracies. Additionally, without removing money from the economy, again, we'd see inflation. So the government would still have incentive to tax in a measured way.

They could stop issuing bonds, as again, they don't need the investment, but people like government bonds. They like having a minimum guaranteed return backed by the security of the government.

How much money is in the vault? Well at one point, Uncle Scrooge knew to the penny. But the government seized it and just put it in a black box labeled "money." And as time passed, it became unnecessary to even believe this box existed. As long as people have faith in the US government and demand for the US dollar, this all works, whether the box is a real vault or electronic ledgers.

posted by explosion at 1:50 PM on June 26, 2019 [9 favorites]

20000 words is a bargain compared to reading Debt: The First 5000 Years, from which this piece clearly draws.

The facinatinating insight for me is how money ultimately derives from systems we created to track our obligations to each other. Paper notes began as sovereign-issued IOUs, whose ultimate authority was that you could pay your taxes with them.

posted by sjswitzer at 1:52 PM on June 26, 2019 [3 favorites]

The facinatinating insight for me is how money ultimately derives from systems we created to track our obligations to each other. Paper notes began as sovereign-issued IOUs, whose ultimate authority was that you could pay your taxes with them.

posted by sjswitzer at 1:52 PM on June 26, 2019 [3 favorites]

All I need to know about modern monetary theory I learned from The Great Eastern, especially Season 3, Episode 11, The Miracle of Economology ... Liquality, Vitality, Tranquility ...

At least it makes as much sense as any of the other insanity.

posted by fimbulvetr at 1:58 PM on June 26, 2019

At least it makes as much sense as any of the other insanity.

posted by fimbulvetr at 1:58 PM on June 26, 2019

All I need to know about modern monetary theory I learned from The Great Eastern

This comment has definitely been the double take of the day for me.

Eight volumes of constant fucking in every possible combination is probably a good analogy for modern monetary theory anyway.

posted by each day we work at 2:15 PM on June 26, 2019

This comment has definitely been the double take of the day for me.

Eight volumes of constant fucking in every possible combination is probably a good analogy for modern monetary theory anyway.

posted by each day we work at 2:15 PM on June 26, 2019

Matt Levine's "Money Stuff" (which is a good free newsletter sub) had a nice potted history of money the other day, as part of an explainer of Facebook's new "Libra" cryptotoken / latest bid for world domination:

Money is a technology. This is true, first of all, in a grand abstract sense: The human capacity to generate collective fictions is our most powerful and general technology, the thing that distinguishes us from other animals and enables long-term cooperation and complex societies, and money is one of the most important collective fictions. Humans were collectively able to decide that discs of shiny metal or sheets of engraved paper could be used as substitutes for all other goods and services, not because they were equivalents of those goods and services but just because we wanted them to be, and this decision created vast new possibilities for storing wealth and planning for the future and motivating human behavior and all the rest.posted by chappell, ambrose at 3:20 PM on June 26, 2019 [11 favorites]

But most of us don’t walk around with a lot of gold coins or even all that much paper money, and the main actual technology of modern money is a bit more prosaic. It is the list. For most people who have money, most of their money consists of an entry in a list at a bank. Each bank has a list of its customers, and next to each customer there’s a number, and that number is the number of dollars that that customer has. It doesn’t, like, correspond to the number of dollars that the customer has; it is not a handy reminder that the bank has a box somewhere with a bunch of gold coins that belong to that customer. There’s no box. The dollars consist solely of the ledger entries at the bank.

This, too, is immensely powerful, especially combined with modern digital technology that lets the bank (and the customer) access the list from anywhere. But there is something too powerful, too easy, about it. The advantage of using gold as money is that it is hard to get a lot of gold: Once everyone agrees that gold is valuable, everyone will want gold, but not everyone will have much of it, so it will retain its value. Once everyone agrees that having a number on a list is valuable, I mean, it’s pretty easy to write a number on a list; right here on my computer I have Microsoft Excel, which allows me to write down long lists of large numbers and put dollar signs in front of them.

So the principal form of modern monetary technology is really legal and regulatory technology. Sure the computer systems that keep the lists of numbers at banks are powerful and complicated, so they don’t mess up the lists, but the thing that keeps the system afloat is mostly a set of rules and norms about who gets to keep lists of numbers of dollars. If your bank says you have some dollars in your checking account, then you do. If I say you have some dollars in my Excel spreadsheet, then you don’t. There is a regulatory privileging of who gets to be a bank, of who gets to be involved in the creation of money. There are central banks that can create money from nothing, and there are regulated banks that can create money under the auspices (and regulation) of the central bank, and there are regulated entities that can transfer and store and otherwise minister to money. Money is just a bunch of computer entries, but it has to be scarce to be valuable, and the computer entries have to reflect a social consensus of who has how much money. And so the structuring and regulation of banking is about making sure that the money is scarce and is allocated in socially approved ways.

Neoliberalism has conned us into fighting climate change as individuals (The Guardian, July 2017) -- While we busy ourselves greening our personal lives, fossil fuel corporations are rendering these efforts irrelevant. The breakdown of carbon emissions since 1988? A hundred companies alone are responsible for an astonishing 71%. You tinker with those pens or that panel; they go on torching the planet. The freedom of these corporations to pollute – and the fixation on a feeble lifestyle response – is no accident. It is the result of an ideological war, waged over the last 40 years, against the possibility of collective action.

Re-situating abortion: Bio-politics, global health and rights in neo-liberal times. (Global Public Health, March 2018) -- New modes of neoliberal and rights-based reproductive governance are emerging across the world which either paradoxically foreclose access to universal health services or promote legislative reform without providing a continuum of services on the ground.

Neoliberal racism: the ‘Southern Strategy’ and the expanding geographies of white supremacy (Social & Cultural Geography, January 2015) -- By connecting the Southern Strategy with a broad economic argument this paper crystallizes the role race plays in the development of the US political economy as well as implications for understanding the way race and capitalism in the USA are co-constituted with one another. Through an examination of the Southern Strategy we can trace both the changing coordinates of the US political economy and race as the USA made the transition from Keynesianism to neoliberalism.

Neoliberalism: the idea that swallowed the world (The Guardian, August 2017) -- Peer through the lens of neoliberalism and you see more clearly how the political thinkers most admired by Thatcher and Reagan helped shape the ideal of society as a kind of universal market (and not, for example, a polis, a civil sphere or a kind of family) and of human beings as profit-and-loss calculators (and not bearers of grace, or of inalienable rights and duties). Of course the goal was to weaken the welfare state and any commitment to full employment, and – always – to cut taxes and deregulate. But “neoliberalism” indicates something more than a standard rightwing wish list. It was a way of reordering social reality, and of rethinking our status as individuals.

Neoliberalism – the ideology at the root of all our problems (The Guardian, April 2016) -- Attempts to limit competition are treated as inimical to liberty. Tax and regulation should be minimised, public services should be privatised. The organisation of labour and collective bargaining by trade unions are portrayed as market distortions that impede the formation of a natural hierarchy of winners and losers. Inequality is recast as virtuous: a reward for utility and a generator of wealth, which trickles down to enrich everyone. Efforts to create a more equal society are both counterproductive and morally corrosive. The market ensures that everyone gets what they deserve.

[Neoliberalism is both a floor wax and a dessert topping.]

posted by Iris Gambol at 3:48 PM on June 26, 2019 [11 favorites]

Re-situating abortion: Bio-politics, global health and rights in neo-liberal times. (Global Public Health, March 2018) -- New modes of neoliberal and rights-based reproductive governance are emerging across the world which either paradoxically foreclose access to universal health services or promote legislative reform without providing a continuum of services on the ground.

Neoliberal racism: the ‘Southern Strategy’ and the expanding geographies of white supremacy (Social & Cultural Geography, January 2015) -- By connecting the Southern Strategy with a broad economic argument this paper crystallizes the role race plays in the development of the US political economy as well as implications for understanding the way race and capitalism in the USA are co-constituted with one another. Through an examination of the Southern Strategy we can trace both the changing coordinates of the US political economy and race as the USA made the transition from Keynesianism to neoliberalism.

Neoliberalism: the idea that swallowed the world (The Guardian, August 2017) -- Peer through the lens of neoliberalism and you see more clearly how the political thinkers most admired by Thatcher and Reagan helped shape the ideal of society as a kind of universal market (and not, for example, a polis, a civil sphere or a kind of family) and of human beings as profit-and-loss calculators (and not bearers of grace, or of inalienable rights and duties). Of course the goal was to weaken the welfare state and any commitment to full employment, and – always – to cut taxes and deregulate. But “neoliberalism” indicates something more than a standard rightwing wish list. It was a way of reordering social reality, and of rethinking our status as individuals.

Neoliberalism – the ideology at the root of all our problems (The Guardian, April 2016) -- Attempts to limit competition are treated as inimical to liberty. Tax and regulation should be minimised, public services should be privatised. The organisation of labour and collective bargaining by trade unions are portrayed as market distortions that impede the formation of a natural hierarchy of winners and losers. Inequality is recast as virtuous: a reward for utility and a generator of wealth, which trickles down to enrich everyone. Efforts to create a more equal society are both counterproductive and morally corrosive. The market ensures that everyone gets what they deserve.

[Neoliberalism is both a floor wax and a dessert topping.]

posted by Iris Gambol at 3:48 PM on June 26, 2019 [11 favorites]

so, neoliberalism is bad?

posted by rude.boy at 3:56 PM on June 26, 2019 [4 favorites]

posted by rude.boy at 3:56 PM on June 26, 2019 [4 favorites]

As long as people have faith in the US government and demand for the US dollar, this all works

I may have spotted a problem

posted by schadenfrau at 4:04 PM on June 26, 2019 [9 favorites]

I may have spotted a problem

posted by schadenfrau at 4:04 PM on June 26, 2019 [9 favorites]

> In fact, banks create money.

Is this no longer taught in high school economics? I distinctly remember thinking it was an incredibly slick trick that banks could loan out something like 10x the amount of money deposited when I learned of this in my high school economics class in the '80s.

posted by smcameron at 5:30 PM on June 26, 2019 [10 favorites]

Is this no longer taught in high school economics? I distinctly remember thinking it was an incredibly slick trick that banks could loan out something like 10x the amount of money deposited when I learned of this in my high school economics class in the '80s.

posted by smcameron at 5:30 PM on June 26, 2019 [10 favorites]

So, if deposits have no connection to the ability of banks to make loans, why do they still take deposits? Even with jacked-up fees, it seems like a pittance compared to the vig on money you can just create from thin air. Is it a requirement of membership in the creating-money club?

Also, which banking entities are allowed to lend money which doesn't yet exist? Credit unions? Those small-town banks that still exist everywhere, like (Your Town) Federal Savings Bank? These modern monetary theory articles always just say "banks".

posted by five toed sloth at 5:50 PM on June 26, 2019 [2 favorites]

Also, which banking entities are allowed to lend money which doesn't yet exist? Credit unions? Those small-town banks that still exist everywhere, like (Your Town) Federal Savings Bank? These modern monetary theory articles always just say "banks".

posted by five toed sloth at 5:50 PM on June 26, 2019 [2 favorites]

So, if deposits have no connection to the ability of banks to make loans, why do they still take deposits? Even with jacked-up fees, it seems like a pittance compared to the vig on money you can just create from thin air. Is it a requirement of membership in the creating-money club?

They do have a connection. Banks can't just arbitrarily lend out infinite money, they have to have assets to back those loans, i.e., deposits. They are required to maintain reserves as well at some percentage of their total assets.

If you deposit $1000 into your bank and the bank has a reserve requirement of 10%, they can lend me $900 (assuming the bank was right at its reserve limit prior to the loan). That money gets credited to my account without being taken out of yours. I have $900, you have $1000, money has been created. Yes, I owe the bank $900, but between you and me we have $1900 of money that we can actually spend on things.

posted by justkevin at 6:17 PM on June 26, 2019 [6 favorites]

They do have a connection. Banks can't just arbitrarily lend out infinite money, they have to have assets to back those loans, i.e., deposits. They are required to maintain reserves as well at some percentage of their total assets.

If you deposit $1000 into your bank and the bank has a reserve requirement of 10%, they can lend me $900 (assuming the bank was right at its reserve limit prior to the loan). That money gets credited to my account without being taken out of yours. I have $900, you have $1000, money has been created. Yes, I owe the bank $900, but between you and me we have $1900 of money that we can actually spend on things.

posted by justkevin at 6:17 PM on June 26, 2019 [6 favorites]

Austerity is bad economics and bad policy, but the kind of thing Mellor's doing isn't really economics or policy at all, and frankly sounds just as muddled and conspiratorial as her gold bug counterparts on the right.

I think you can arrive at very liberal and even leftist policy goals just by focusing on rent seeking and corruption. The social history of currency and debt really doesn't have much to do with it. And at this point the word "neoliberal" has been used to mean so many different things that we should just retire the term.

posted by neat graffitist at 6:44 PM on June 26, 2019 [3 favorites]

I think you can arrive at very liberal and even leftist policy goals just by focusing on rent seeking and corruption. The social history of currency and debt really doesn't have much to do with it. And at this point the word "neoliberal" has been used to mean so many different things that we should just retire the term.

posted by neat graffitist at 6:44 PM on June 26, 2019 [3 favorites]

If your bank says you have some dollars in your checking account, then you do. If I say you have some dollars in my Excel spreadsheet, then you don’t. There is a regulatory privileging of who gets to be a bank, of who gets to be involved in the creation of money.

Interestingly, there's much less regulatory privileging of who gets to create negative money, i.e. debt.

If you say I have some negative dollars in your Excel spreadsheet, I'm pretty much on my own if I want to dispute that.

posted by HiroProtagonist at 7:35 PM on June 26, 2019 [2 favorites]

Interestingly, there's much less regulatory privileging of who gets to create negative money, i.e. debt.

If you say I have some negative dollars in your Excel spreadsheet, I'm pretty much on my own if I want to dispute that.

posted by HiroProtagonist at 7:35 PM on June 26, 2019 [2 favorites]

I don’t think we should retire a term that has use just cause other people misuse it but I sometimes use neoliberalism to talk about “market fundamentalism” and how it operates more as articles of faith then economic theory.

posted by The Whelk at 7:36 PM on June 26, 2019

posted by The Whelk at 7:36 PM on June 26, 2019

I think a lot of people say neoliberalism when they just mean capitalism, because that gives the audience the space to imagine that there was a functional capitalism at some point we can return to.

posted by AnhydrousLove at 7:40 PM on June 26, 2019 [3 favorites]

posted by AnhydrousLove at 7:40 PM on June 26, 2019 [3 favorites]

Well there’s an argument it’s just a return to an earlier form of capitalistic thought that gave us the crisises and depressions of the 19th and early 20th centuries and the mid century regulatory state was a brief cease fire in the class war and they needed a new word cause they couldn’t say “what Calvin Coolidge did”

posted by The Whelk at 8:03 PM on June 26, 2019 [2 favorites]

posted by The Whelk at 8:03 PM on June 26, 2019 [2 favorites]

But neoliberalism as expressed by “the policies of Reagan and Thatcher and Pinochet” Have a much more international and militaristic flare then say, Warren Harding.

posted by The Whelk at 8:12 PM on June 26, 2019

posted by The Whelk at 8:12 PM on June 26, 2019

Forget about money. Let's start with a fundamental truth: If an economy is operating at potential - that is, full employment and capital utilization - then if you want to use some resources for governmental purposes, less resources will be available for other purposes. That may or may not be a good idea, but (in the short term) you can't create resources out of thin air.

That is completely separate from the truth that in a recession, fiscal stimulus can create wealth, because it increases utilization of available resources, such as unemployed workers. Austerity during the last recession was a massive policy failure. But that is just what Keynes observed nearly a century ago.

Ughh.

posted by Mr.Know-it-some at 8:22 PM on June 26, 2019

That is completely separate from the truth that in a recession, fiscal stimulus can create wealth, because it increases utilization of available resources, such as unemployed workers. Austerity during the last recession was a massive policy failure. But that is just what Keynes observed nearly a century ago.

Ughh.

posted by Mr.Know-it-some at 8:22 PM on June 26, 2019

I find it a bit odd that there's not one mention of inflation in the article. Weimar Germany knew where money comes from and their printing banknotes didn't help them. Thanks, Explosion, for bringing it into the discussion.

Our current economic problem is a shift in wealth ownership to a very few people. The "handbag economics" metaphor is a framework used in the US to limit government expenditures to the majority of people. "Trickle down" and the "Laffer curve" limit taxation of the wealthy ("job creators"). Inflation is held in check by monitoring and punishing wage growth. All of this has the effect of shifting wealth to the people who don't spend it (limiting economic growth) and don't need it (they already own 70% of the country anyway). The past two decades we've struggled to reach a 2% inflation target because nobody is getting a raise. Meanwhile we get asset bubbles and hedge funds because the rich can't keep up with the growth in their money.

I lay the blame for these on Volker and Greenspan and Business Schools. Politicians aren't experts and they'll use motivated reasoning to accept any garbage that allows them to give wealth to the people that line their pockets. It's the academics that should understand their role in upward wealth redistribution.

posted by Emmy Noether at 8:38 PM on June 26, 2019 [4 favorites]

Our current economic problem is a shift in wealth ownership to a very few people. The "handbag economics" metaphor is a framework used in the US to limit government expenditures to the majority of people. "Trickle down" and the "Laffer curve" limit taxation of the wealthy ("job creators"). Inflation is held in check by monitoring and punishing wage growth. All of this has the effect of shifting wealth to the people who don't spend it (limiting economic growth) and don't need it (they already own 70% of the country anyway). The past two decades we've struggled to reach a 2% inflation target because nobody is getting a raise. Meanwhile we get asset bubbles and hedge funds because the rich can't keep up with the growth in their money.

I lay the blame for these on Volker and Greenspan and Business Schools. Politicians aren't experts and they'll use motivated reasoning to accept any garbage that allows them to give wealth to the people that line their pockets. It's the academics that should understand their role in upward wealth redistribution.

posted by Emmy Noether at 8:38 PM on June 26, 2019 [4 favorites]

the answer to the expanding inflation of 1976 and onwards was not to raise wages but to expland access to easy credit for everyone, kick the can into the future, into now where basically no familiy under 35 has any wealth to speak of when you factor debt in

posted by The Whelk at 8:47 PM on June 26, 2019 [1 favorite]

posted by The Whelk at 8:47 PM on June 26, 2019 [1 favorite]

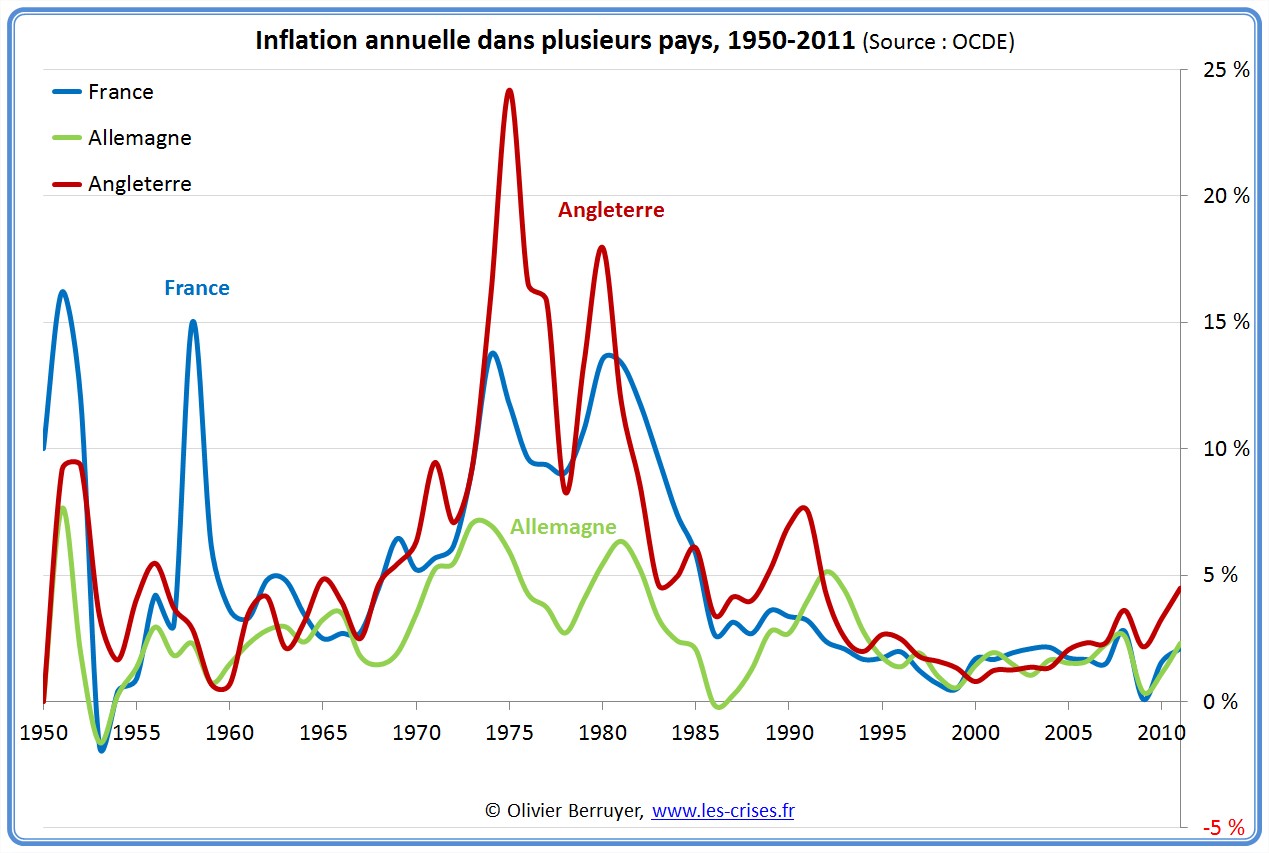

Yeah, it's a little weird for the article not to even admit that inflation can be a problem. It's not that long ago-- namely, 1975-- that inflation in the UK approached 25%. In the US it stayed under 14%, still enough to annoy people... that's how we got neoliberalism.

But otherwise, the takedown of neoliberalism is very welcome. People are way too deferential to what Paul Krugman calls the "Very Serious People", the ones who are terribly worried about debt under Democratic presidents and who spent the 2010s predicting hyperinflation.

Adam Smith actually pointed out 250 years ago-- in a passage possibly skipped over by his present-day admirers-- that the well-off actually like and prefer bad times. It keeps workers from making pesky demands for more money and makes both business and government avoid big projects that might upset the status quo.

posted by zompist at 8:59 PM on June 26, 2019 [3 favorites]

{kind=link}

{kind=link}

But otherwise, the takedown of neoliberalism is very welcome. People are way too deferential to what Paul Krugman calls the "Very Serious People", the ones who are terribly worried about debt under Democratic presidents and who spent the 2010s predicting hyperinflation.

Adam Smith actually pointed out 250 years ago-- in a passage possibly skipped over by his present-day admirers-- that the well-off actually like and prefer bad times. It keeps workers from making pesky demands for more money and makes both business and government avoid big projects that might upset the status quo.

posted by zompist at 8:59 PM on June 26, 2019 [3 favorites]

Collapses and depressions are great for the big holders of capital cause it rids the field of competitors who can now be bought up cheap, there's a reason the great bubble machine never stops, and even Adam Smith with talk about companies will always become monopolies that conspire against the public without intense regulation gets called a "proto-marxist" by the more rabid and serious market fundamentalists

posted by The Whelk at 9:20 PM on June 26, 2019 [2 favorites]

posted by The Whelk at 9:20 PM on June 26, 2019 [2 favorites]

if you want to use some resources for governmental purposes, less resources will be available for other purposes.

That's pretty much tautological. If you want to use some resources for ANY purposes, less resources will be available for other purposes.

There's nothing particularly special about "governmental purposes", but what makes a big difference is this:

Is the government serving the people, or are the people serving the government?

Thus one countries experience will differ from another.

posted by HiroProtagonist at 10:21 PM on June 26, 2019 [3 favorites]

That's pretty much tautological. If you want to use some resources for ANY purposes, less resources will be available for other purposes.

There's nothing particularly special about "governmental purposes", but what makes a big difference is this:

Is the government serving the people, or are the people serving the government?

Thus one countries experience will differ from another.

posted by HiroProtagonist at 10:21 PM on June 26, 2019 [3 favorites]

This topic always weirds me out because people seem treat the idea that banks 'create money' as if it is terribly strange and profound, and never mention the corresponding half of the equation.

That money gets credited to my account without being taken out of yours. I have $900, you have $1000, money has been created. Yes, I owe the bank $900, but between you and me we have $1900 of money that we can actually spend on things.

But then, doesn't money get destroyed when you repay your loan? I mean, sure, the bank gets to keep the interest component, but the principal just sorta goes *poof* into thin air.

...Right?

...Am I missing something?

posted by colin.jaquiery at 3:06 AM on June 27, 2019

That money gets credited to my account without being taken out of yours. I have $900, you have $1000, money has been created. Yes, I owe the bank $900, but between you and me we have $1900 of money that we can actually spend on things.

But then, doesn't money get destroyed when you repay your loan? I mean, sure, the bank gets to keep the interest component, but the principal just sorta goes *poof* into thin air.

...Right?

...Am I missing something?

posted by colin.jaquiery at 3:06 AM on June 27, 2019

Also, not to derail, but is there a name for the 4th quadrant in the spend/tax 2-by-2?

Progressive: Spend lots and tax lots.

Conservative: Spend as little as possible, tax even less.

Modern Monetary Theorist: Just spend lots. She'll be right.

???: Take every last dollar AND BURN IT.

posted by colin.jaquiery at 3:15 AM on June 27, 2019 [1 favorite]

Progressive: Spend lots and tax lots.

Conservative: Spend as little as possible, tax even less.

Modern Monetary Theorist: Just spend lots. She'll be right.

???: Take every last dollar AND BURN IT.

posted by colin.jaquiery at 3:15 AM on June 27, 2019 [1 favorite]

Why would it disappear?

posted by lokta at 5:36 AM on June 27, 2019 [1 favorite]

posted by lokta at 5:36 AM on June 27, 2019 [1 favorite]

Does anyone know whether banks DO effectively delete the principal component of loan repayments, rather than considering it new cash to back further loans? It seems as though it would be a very basic requirement of double-entry bookkeeping, but who knows what implausible things might go on in the real world...

posted by Nutri-Matic Drinks Synthesizer at 5:47 AM on June 27, 2019

posted by Nutri-Matic Drinks Synthesizer at 5:47 AM on June 27, 2019

Also, not to derail, but is there a name for the 4th quadrant in the spend/tax 2-by-2?

Centrism.

posted by Ptrin at 6:28 AM on June 27, 2019

Centrism.

posted by Ptrin at 6:28 AM on June 27, 2019

Progressive: Spend lots and tax lots.

Conservative: Spend as little as possible, tax even less.

Those cliches do not hold up to facts.

posted by fimbulvetr at 6:56 AM on June 27, 2019 [4 favorites]

Conservative: Spend as little as possible, tax even less.

Those cliches do not hold up to facts.

posted by fimbulvetr at 6:56 AM on June 27, 2019 [4 favorites]

Neoliberalism has also tricked us about where work comes from. (I mean, calling wealthy hedge fund managers and private equity pirates "job creators" hahaha oof.)

posted by zenzenobia at 7:10 AM on June 27, 2019 [5 favorites]

posted by zenzenobia at 7:10 AM on June 27, 2019 [5 favorites]

Neoliberalism seems to be all about dehumanization and extraction of value. Which reminds me a little bit of the Matrix, where humanity is literally farmed for … something.

posted by ZeusHumms at 8:42 AM on June 27, 2019 [2 favorites]

posted by ZeusHumms at 8:42 AM on June 27, 2019 [2 favorites]

Well one of the definitions of late stage capitalism is when there are no more frontiers and borderlands to extract from so it turns inwards and starts extracting wealth out of itself, much like how the brutal militarism of the colonies came home to Europe in the First World War .

posted by The Whelk at 9:17 AM on June 27, 2019 [3 favorites]

posted by The Whelk at 9:17 AM on June 27, 2019 [3 favorites]

Why would it disappear?

This is absolutely not my wheelhouse - and frankly trying to write this out has made it painfully clear to me just how muddy my own thinking on this is - so please take everything I am about to say with a mountain of salt. That said, I will offer you a short, pleasant answer and a long, boring answer.

a) Because it is leprechaun gold and the goblin bankers will take one look and call it out as such.

b) Because when hand wavy pundits say that banks create money, they are paraphrasing - poorly - economists who say that banks issuing loans increases M1 money supply (broad money).

When banks issue you a loan they create two records. One record says that you, the customer, owe the bank money to the value of the loan. The other record says that you, the customer, have a deposit with the bank to the value of the loan. These records are created at the same time, and are alternately assets and liabilities for both you and the bank. Your net worth has not changed. Nor has the net worth of the bank. Nobody outside you and the bank knows about the transaction and - for the moment - nobody cares.

Nevertheless, you now have access to a money supply that did not exist previously. You could go to the cornershop, cut a cheque, and enjoy a crispy cool soda. Nice!

Of course, supposing you do this, when the owner of the cornershop cashes your check the bank will reduce the value of your deposit by the cost of the soda. The owner gets to increase their deposit in their bank by the same amount though, so the supply of money hasn't been reduced - you can access less money, they can access more. Everything is balanced and all is right in the world.

By lending you money, the bank has increased your access to money. (Kinda a truism, huh.)

But suppose you balk at your newfound freedom. So much choice! You haven't even made it out the door before you turn around, walk back to the loan manager and ask to settle your debt. "We can do that." She says. The bank takes that record that says you have a deposit with the bank together with that record that says you have a loan with the bank and cancels them against each other. And *poof!* Your net worth has not changed. Nor has the net worth of the bank. But suddenly you don't have access to that money anymore.

You have to write down a deposit to settle a loan, and deposits are counted as part of money supply.

Money supply, in this sense, is the sum of all the cash money and accounts that somebody could conceivably spend on something without disturbing the tortuous web of nested obligations underlying the global financial system.

Issuing new loans and deposits increases money supply. The inverse operation reduces money supply.

---

Money supply can be a really useful concept for thinking about problems in economics.

(Delightfully, scriptural money can be thought of as analogous to actual currency issued by states. I really like that.)

Does money supply really help us understand whether Thatcheresque austerity measures will or won't help bring about the best of all possible worlds?

Ehh.

posted by colin.jaquiery at 5:51 AM on June 28, 2019

This is absolutely not my wheelhouse - and frankly trying to write this out has made it painfully clear to me just how muddy my own thinking on this is - so please take everything I am about to say with a mountain of salt. That said, I will offer you a short, pleasant answer and a long, boring answer.

a) Because it is leprechaun gold and the goblin bankers will take one look and call it out as such.

b) Because when hand wavy pundits say that banks create money, they are paraphrasing - poorly - economists who say that banks issuing loans increases M1 money supply (broad money).

When banks issue you a loan they create two records. One record says that you, the customer, owe the bank money to the value of the loan. The other record says that you, the customer, have a deposit with the bank to the value of the loan. These records are created at the same time, and are alternately assets and liabilities for both you and the bank. Your net worth has not changed. Nor has the net worth of the bank. Nobody outside you and the bank knows about the transaction and - for the moment - nobody cares.

Nevertheless, you now have access to a money supply that did not exist previously. You could go to the cornershop, cut a cheque, and enjoy a crispy cool soda. Nice!

Of course, supposing you do this, when the owner of the cornershop cashes your check the bank will reduce the value of your deposit by the cost of the soda. The owner gets to increase their deposit in their bank by the same amount though, so the supply of money hasn't been reduced - you can access less money, they can access more. Everything is balanced and all is right in the world.

By lending you money, the bank has increased your access to money. (Kinda a truism, huh.)

But suppose you balk at your newfound freedom. So much choice! You haven't even made it out the door before you turn around, walk back to the loan manager and ask to settle your debt. "We can do that." She says. The bank takes that record that says you have a deposit with the bank together with that record that says you have a loan with the bank and cancels them against each other. And *poof!* Your net worth has not changed. Nor has the net worth of the bank. But suddenly you don't have access to that money anymore.

You have to write down a deposit to settle a loan, and deposits are counted as part of money supply.

Money supply, in this sense, is the sum of all the cash money and accounts that somebody could conceivably spend on something without disturbing the tortuous web of nested obligations underlying the global financial system.

Issuing new loans and deposits increases money supply. The inverse operation reduces money supply.

---

Money supply can be a really useful concept for thinking about problems in economics.

(Delightfully, scriptural money can be thought of as analogous to actual currency issued by states. I really like that.)

Does money supply really help us understand whether Thatcheresque austerity measures will or won't help bring about the best of all possible worlds?

Ehh.

posted by colin.jaquiery at 5:51 AM on June 28, 2019

The extra thing here is that the bank can loan you money that didn't exist before it was loaned to you. So treating things like a balanced household budget is factually incorrect. And Thatcher style austerity is nonsensical if there's no fixed amount of currency.

We can argue about her much inflation we are ok with, or which structural incentives are most helpful.

But the very premise of austerity, and applying household budget logic to nations generally, is absurd.

posted by idiopath at 10:43 PM on June 28, 2019

We can argue about her much inflation we are ok with, or which structural incentives are most helpful.

But the very premise of austerity, and applying household budget logic to nations generally, is absurd.

posted by idiopath at 10:43 PM on June 28, 2019

Breaking it down further: we print money, in a way that most directly benefits two groups: the bank owners and people approved for loans. In aggregate, the rich.

We then use that printing of money to justify cutting services, which primarily hurts the poor. And the reduced economic activity from cutting those expenditures slows the economy and further accentuates the need for those services being cut.

On all sides of the dynamic, inequality is ratcheted further.

posted by idiopath at 10:55 PM on June 28, 2019

We then use that printing of money to justify cutting services, which primarily hurts the poor. And the reduced economic activity from cutting those expenditures slows the economy and further accentuates the need for those services being cut.

On all sides of the dynamic, inequality is ratcheted further.

posted by idiopath at 10:55 PM on June 28, 2019

If you only print money for private business, and treat government spending like a household zero balance budget, you can only "afford" social services when they are least needed, by looping the money through business loans back into taxes paid.

(assuming we even attempt to do that - cruel tax enforcement that only enforces taxes for the poor makes this even worse still)

When people need the services most, the elitist bean counters announce the budget must shrink. The same ones who decided private banks could print money.

posted by idiopath at 11:10 PM on June 28, 2019 [1 favorite]

(assuming we even attempt to do that - cruel tax enforcement that only enforces taxes for the poor makes this even worse still)

When people need the services most, the elitist bean counters announce the budget must shrink. The same ones who decided private banks could print money.

posted by idiopath at 11:10 PM on June 28, 2019 [1 favorite]

"So treating things like a balanced household budget is factually incorrect."

"...if there's no fixed amount of currency."

Ehh, look. I disagree with you on the terminology and semantics but...

"On all sides of the dynamic, inequality is ratcheted further."

Amen.

posted by colin.jaquiery at 4:59 AM on June 29, 2019

"...if there's no fixed amount of currency."

Ehh, look. I disagree with you on the terminology and semantics but...

"On all sides of the dynamic, inequality is ratcheted further."

Amen.

posted by colin.jaquiery at 4:59 AM on June 29, 2019

> Unlike sovereign money, which was created and spent directly into circulation, modern money is largely borrowed into circulation through the banking system. This process shelters behind another myth, that banks merely act as a link between savers and borrowers. In fact, banks create money. And it is only in the last decade that this powerful myth has been finally put to rest by banking and monetary authorities.

It is now acknowledged by monetary authorities such as the IMF, the US Federal Reserve and the Bank of England, that banks are creating new money when they make loans. They don’t lend the money of other account holders to those who want to borrow.

Bank loans consist of money conjured out of thin air, whereby new money is credited to the borrowers account with the agreement that the amount will eventually be repaid with interest.

A lost century in economics: Three theories of banking and the conclusive evidence

> Matt Levine's "Money Stuff" (which is a good free newsletter sub) had a nice potted history of money the other day, as part of an explainer of Facebook's new "Libra" cryptotoken / latest bid for world domination:

previously :P

posted by kliuless at 12:41 AM on June 30, 2019 [2 favorites]

It is now acknowledged by monetary authorities such as the IMF, the US Federal Reserve and the Bank of England, that banks are creating new money when they make loans. They don’t lend the money of other account holders to those who want to borrow.

Bank loans consist of money conjured out of thin air, whereby new money is credited to the borrowers account with the agreement that the amount will eventually be repaid with interest.

A lost century in economics: Three theories of banking and the conclusive evidence

- The three theories of how banks function and whether they create money are reviewed

- A new empirical test of the three theories is presented

- The test allows to control for all transactions, delivering clear-cut results

- The fractional reserve and financial intermediation theories of banking are rejected

- Capital adequacy based bank regulation is ineffective, credit guidance preferable

- This is shown with the case study of Barclays Bank creating its own capital

- Questions are raised concerning the lack of progress in economics in the past century

- Policy implications: borrowing from abroad is unnecessary for growth

How do banks operate and where does the money supply come from? The financial crisis has heightened awareness that these questions have been unduly neglected by many researchers. During the past century, three different theories of banking were dominant at different times: (1) The currently prevalent financial intermediation theory of banking says that banks collect deposits and then lend these out, just like other non-bank financial intermediaries. (2) The older fractional reserve theory of banking says that each individual bank is a financial intermediary without the power to create money, but the banking system collectively is able to create money through the process of ‘multiple deposit expansion’ (the ‘money multiplier’). (3) The credit creation theory of banking, predominant a century ago, does not consider banks as financial intermediaries that gather deposits to lend out, but instead argues that each individual bank creates credit and money newly when granting a bank loan. The theories differ in their accounting treatment of bank lending as well as in their policy implications. Since according to the dominant financial intermediation theory banks are virtually identical with other non-bank financial intermediaries, they are not usually included in the economic models used in economics or by central bankers. Moreover, the theory of banks as intermediaries provides the rationale for capital adequacy-based bank regulation. Should this theory not be correct, currently prevailing economics modelling and policy-making would be without empirical foundation. Despite the importance of this question, so far only one empirical test of the three theories has been reported in learned journals. This paper presents a second empirical test, using an alternative methodology, which allows control for all other factors. The financial intermediation and the fractional reserve theories of banking are rejected by the evidence. This finding throws doubt on the rationale for regulating bank capital adequacy to avoid banking crises, as the case study of Credit Suisse during the crisis illustrates. The finding indicates that advice to encourage developing countries to borrow from abroad is misguided. The question is considered why the economics profession has failed over most of the past century to make any progress concerning knowledge of the monetary system, and why it instead moved ever further away from the truth as already recognised by the credit creation theory well over a century ago. The role of conflicts of interest and interested parties in shaping the current bank-free academic consensus is discussed. A number of avenues for needed further research are indicated.or as explained here![1,2]

> Matt Levine's "Money Stuff" (which is a good free newsletter sub) had a nice potted history of money the other day, as part of an explainer of Facebook's new "Libra" cryptotoken / latest bid for world domination:

previously :P

posted by kliuless at 12:41 AM on June 30, 2019 [2 favorites]

« Older Motion capture madness | Delta Delta Delta, can I help ya help ya help ya? Newer »

This thread has been archived and is closed to new comments

posted by sammyo at 1:08 PM on June 26, 2019 [2 favorites]