"There needs to be a general acceptance that the current model has failed."

May 26, 2009 1:10 PM Subscribe

It's Finished is a witty and erudite essay by MeFi lurker John Lanchester in The London Review of Books on how completely and utterly screwed the British economy is. In the process of laying out his case Lanchester touches on varied issues, such Scottish banknotes, why Alan Hollinghurst's phrase "tremendous, Basil Fawltyish lengths" is applicable to the reaction by the US and UK governments to the banking meltdown, the value destruction of corporate mergers, the invention of modern accounting, and why no one really knows how large a share of the failed banks is owned by governments.

This must be the first time I've left my computer to read a link.

posted by Elmore at 1:29 PM on May 26, 2009

posted by Elmore at 1:29 PM on May 26, 2009

“…so far taxpayers have spent £45.5 billion in directly bailing out RBS (for wonks, that’s £15 billion in equity and £5 billion in preference shares last October, followed by £25.5 billion in capital instruments this February), plus another £50 billion for the toxic assets in the protection scheme”

Well to be fair the British economy hasn’t bludgeoned any charismatic preachers to death with a bowling pin… as far as we know.

Pretty bleak tho.

posted by Smedleyman at 1:31 PM on May 26, 2009 [1 favorite]

Well to be fair the British economy hasn’t bludgeoned any charismatic preachers to death with a bowling pin… as far as we know.

Pretty bleak tho.

posted by Smedleyman at 1:31 PM on May 26, 2009 [1 favorite]

Thanks for this. Very long but a good read. I sent the link to my accountant! I always say to him "This is what I earned this year. Now what do you say I earned?" Of course I always go with his answer. I fully appreciate the connection between accounting and magic.

posted by binturong at 1:40 PM on May 26, 2009

posted by binturong at 1:40 PM on May 26, 2009

Smedleyman: "“ the British economy hasn’t bludgeoned any charismatic preachers to death with a bowling pin… as far as we know."

If "Basil Fawltyish" is the correct adjective, we would expect it to perform its killings with spoiled kippers instead.

posted by Joe Beese at 1:40 PM on May 26, 2009

If "Basil Fawltyish" is the correct adjective, we would expect it to perform its killings with spoiled kippers instead.

posted by Joe Beese at 1:40 PM on May 26, 2009

I wish this article was broken up into chunks on different pages.

posted by smackfu at 2:06 PM on May 26, 2009

posted by smackfu at 2:06 PM on May 26, 2009

It's quite the slog, well written though it is, and tough to absorb. And as depressing as all fuck, in a cheery, witty kind of way. I'm actually only half way in, and quite gloomy about it. Still, if I could favorite it more than once I totally would.

posted by Artw at 2:08 PM on May 26, 2009

posted by Artw at 2:08 PM on May 26, 2009

If we’re lucky, it won’t be any worse than Thatcherism.

Sigh. Are we at least gonna get some decent music out of this current catastrophe? I've still got my skinny ties!

posted by The Whelk at 2:17 PM on May 26, 2009 [4 favorites]

Sigh. Are we at least gonna get some decent music out of this current catastrophe? I've still got my skinny ties!

posted by The Whelk at 2:17 PM on May 26, 2009 [4 favorites]

Read that a couple of days ago. Lancaster, who's always good value, wrote about a good article about the crash last year.

I kinda think/hope he DOOMified up the figures at the end. Though even best cast scenario ain't gonna be pleasent.

posted by fearfulsymmetry at 2:28 PM on May 26, 2009

I kinda think/hope he DOOMified up the figures at the end. Though even best cast scenario ain't gonna be pleasent.

posted by fearfulsymmetry at 2:28 PM on May 26, 2009

Are we at least gonna get some decent music out of this current catastrophe?

Fingers crossed for another Alan Moore.

posted by Artw at 2:30 PM on May 26, 2009

Fingers crossed for another Alan Moore.

posted by Artw at 2:30 PM on May 26, 2009

Hmm. I don't like bits like this:

"SIVs involved borrowing short in order to lend long, the same dazzlingly successful financial model that underpinned Northern Rock"

Retail banking in general involves borrowing short (taking deposits) and lending long (issuing mortgages). It's not a terrible business per se. This was a cheap shot that undermines credibility.

posted by i_am_joe's_spleen at 2:32 PM on May 26, 2009

"SIVs involved borrowing short in order to lend long, the same dazzlingly successful financial model that underpinned Northern Rock"

Retail banking in general involves borrowing short (taking deposits) and lending long (issuing mortgages). It's not a terrible business per se. This was a cheap shot that undermines credibility.

posted by i_am_joe's_spleen at 2:32 PM on May 26, 2009

Wow that's 14K (or so) interesting words, to say pretty much (although coming at it from a different direction) what Jim Rogers said in about 900 words last January: "I would urge you to sell any sterling you might have. It's finished. I hate to say it, but I would not put any money in the UK."

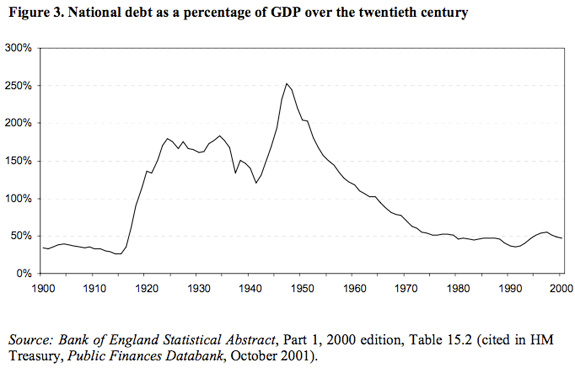

Each conclusion is interesting for different reasons. Both express concern about the size of the UK debt, relative to GDP, with Lanchester mentioning that "National debt will hit 79 per cent of GDP".

But just to reinforce my oft stated motto one should always apply to the markets - all predictions are wrong - we see that in mid February UK national debt is set to surpass £2 trillion, or about 150% of GDP.

How does this sit in historical terms? Well, certainly bad but not the end of the world; we can see that right after WWII UK debt as percentage of GDP approached 250%.

The big concern here of course is deflation, which increases the burden debt in real terms. But not to worry; all of the incessant predictions warning us of rocketing inflation have, to date, proved wrong as deflation seems to be ruling the day (for now) with RPI actually turning negative in March 2009. However that will change soon enough, once the truly massive deflationary forces buffeting the economy have waned.

And The Pound you might ask? Well, after dropping some twenty odd percent against a basket of other currencies over the past year, now many analysts are actually suggesting that its undervalued, with Goldman forecasting "a 23 percent gain versus the dollar and 15 percent advance against the euro."

So there you go. Lots of conflicting information to be sure. About the only takeaway would be all predictions are wrong, and the global economy is a bafflingly large and inscrutable beast over a sufficiently long horizon.

You ask me how to make money over the next twenty years? I have no idea, but I can decompose that into eighty smaller problems, and fairly consistently make money quarter to quarter. I'm not sure anyone can accurately and consistently predict which way the global financial system is gonna go year by year. So I don't take much stock in the long term, definitive predictions.

After all, I'd suggest that it's finished is more a relative term than anything else. Finished compared to what other nation?

That being said, I haven't sold any shares since long before all this fun kicked off, I'm still long gold & silver (just bought more physical silver here in London last week, and I'm trying to source physical gold but it is still difficult to consistently obtain), and diversified - although not as much as I'd like - between the US Dollar, The Pound, The Aussie Dollar and I'm looking for a clean way to get some Swiss Franc exposure as well.

'Cause nobody really knows what the hell is gonna happen.

Many thanks for posting - I'm half asleep (long day, I'm usually up at 5:30AM) but managed to get through it once. I'm the kind of reader that has to go over things a couple of times so I'll hit it again in the AM. Thanks again for posting - I certainly wouldn't have seen it otherwise.

posted by Mutant at 2:34 PM on May 26, 2009 [12 favorites]

Each conclusion is interesting for different reasons. Both express concern about the size of the UK debt, relative to GDP, with Lanchester mentioning that "National debt will hit 79 per cent of GDP".

But just to reinforce my oft stated motto one should always apply to the markets - all predictions are wrong - we see that in mid February UK national debt is set to surpass £2 trillion, or about 150% of GDP.

How does this sit in historical terms? Well, certainly bad but not the end of the world; we can see that right after WWII UK debt as percentage of GDP approached 250%.

{kind=link}

The big concern here of course is deflation, which increases the burden debt in real terms. But not to worry; all of the incessant predictions warning us of rocketing inflation have, to date, proved wrong as deflation seems to be ruling the day (for now) with RPI actually turning negative in March 2009. However that will change soon enough, once the truly massive deflationary forces buffeting the economy have waned.

And The Pound you might ask? Well, after dropping some twenty odd percent against a basket of other currencies over the past year, now many analysts are actually suggesting that its undervalued, with Goldman forecasting "a 23 percent gain versus the dollar and 15 percent advance against the euro."

So there you go. Lots of conflicting information to be sure. About the only takeaway would be all predictions are wrong, and the global economy is a bafflingly large and inscrutable beast over a sufficiently long horizon.

You ask me how to make money over the next twenty years? I have no idea, but I can decompose that into eighty smaller problems, and fairly consistently make money quarter to quarter. I'm not sure anyone can accurately and consistently predict which way the global financial system is gonna go year by year. So I don't take much stock in the long term, definitive predictions.

After all, I'd suggest that it's finished is more a relative term than anything else. Finished compared to what other nation?

That being said, I haven't sold any shares since long before all this fun kicked off, I'm still long gold & silver (just bought more physical silver here in London last week, and I'm trying to source physical gold but it is still difficult to consistently obtain), and diversified - although not as much as I'd like - between the US Dollar, The Pound, The Aussie Dollar and I'm looking for a clean way to get some Swiss Franc exposure as well.

'Cause nobody really knows what the hell is gonna happen.

Many thanks for posting - I'm half asleep (long day, I'm usually up at 5:30AM) but managed to get through it once. I'm the kind of reader that has to go over things a couple of times so I'll hit it again in the AM. Thanks again for posting - I certainly wouldn't have seen it otherwise.

posted by Mutant at 2:34 PM on May 26, 2009 [12 favorites]

Jesus, I thought you were saying that Lanchester was a MeFi member, and I was about to start screaming like a teenage girl at a Beatles concert.

posted by Ian A.T. at 2:43 PM on May 26, 2009

posted by Ian A.T. at 2:43 PM on May 26, 2009

Mutant: Might be worth buying some NOK as well? The Swiss have a little problem called UBS, whereas the Norwegians are still sitting on a large pile of oil.

posted by pharm at 2:45 PM on May 26, 2009

posted by pharm at 2:45 PM on May 26, 2009

I got about 1/3 of the way through the article when I hit his example of a balance sheet:

posted by mr vino at 2:47 PM on May 26, 2009

Assets Share of house owned by me £70,000 Deposits in bank £10,000 Car £10,000 Stuff I own £15,000 Money people owe me £5,000 Pension £40,000 Total £150,000 Liabilities Share of house owned by bank £130,000 Credit card debt £2,000 Car loan £2,000 Unpaid debt on stuff I own £6,000 Total £140,000 Equity £10,000 Total Liabilities and Equity £150,000The entries for the house are nonsense: if I own a £200,000 house, and owe £130,000 on it, then I've got £70,000 in equity on the house - not, as this implies, a £60,000 net liability. He does seem to get it right for "stuff I own" vs "Unpaid debt on stuff I own," but this doesn't make me want to read anything else he has to say about balance sheets, or finance in general for that matter.

posted by mr vino at 2:47 PM on May 26, 2009

mr vino if I own a £200,000 house, and owe £130,000 on it, then I've got £70,000 in equity on the house

Erm. Let's say the value of the house drops to £100,000. What is your net equity now? The same? Even though you've still got the £200,000 mortgage?

posted by crayz at 2:55 PM on May 26, 2009

Erm. Let's say the value of the house drops to £100,000. What is your net equity now? The same? Even though you've still got the £200,000 mortgage?

posted by crayz at 2:55 PM on May 26, 2009

Wow, there's a lot going on in that piece. Touches on a lot of issues, but appropriately so since they're all related.

They would not be sacrificing the bank at the altar of Public Good, they'd have to sacrifice themselves and their careers, their hopes of ever being elected again, if they wanted to run a major bank effectively.

This reason completely trumps the sort of 'national pride' that he gives as #4; although I agree that there is a degree of Ango-Saxon capitalist pride that cries out against nationalizing anything, the elites in both the U.K. and U.S. are not the sorts to let anything as old-fashioned as pride or ideals or ethics to stand in the way of practical business. There's just no political will to do it: the last thing Congress wants to do is add "running a bank" to its list of troubles. (Given the fact that many of them are lawyers by profession in addition to being politicians, a bank nationalization would put them in line for the people-the-public-loves-to-hate trifecta.)

There are a couple of things here and there that I don't quite agree with, or perhaps just don't understand:

Does Britain have a prohibition against debt monetization that the U.S. does not? And if it does, is it realistic to expect that prohibition to remain in place in such a scenario? I'm skeptical.

posted by Kadin2048 at 3:06 PM on May 26, 2009 [2 favorites]

It isn't hard to know how to slay the [insolvent "zombie banks"]. The only way to do it is to hold a gun to the head of the various bankers – those various guys sitting with their heads in their hands staring at balance sheets with holes in them – and force them to admit what their assets are worth, right now. Many of the banks will turn out to be insolvent. In that case the bank is nationalised, or at the very least goes into administration and receivership. […]I think he nails it there. Also, when he discusses the reasons why nationalization isn't being seriously considered, I think he's onto something again:

Nobody in power wants to do that. Nobody with power in the banking system, and nobody with power in government. Both the British and the American plans to help the banks are very, very, very expensive variations on the theme of sticking their fingers in their ears and loudly singing ‘La la la, I'm not listening.’

Because if the banks were taken over, then every decision they take would come at a potential political cost to the government. Your state-owned mortgage lender is threatening to repossess your house, after you fell behind on the payments? Blame the government. Your firm is laying off half its workforce because the bank won’t roll over its loan? Blame the government. This, of course, is in addition to all the other economic things for which people are already blaming the government. People are grumbling now, but to nothing like the extent they would if the banks were directly owned by the state. Politicians simply aren’t willing to take on the responsibility for the banks’ actions.That right there is why you'll never see nationalization. Everything else is window dressing, at least here in the U.S.; all the talk of "socialism" versus the market economy and capitalism is meaningless. We have government monopolies in other areas, have had them historically, and it has not killed capitalism; the reason the government won't take over the banks is because the politicians don't have the stomach for it.

They would not be sacrificing the bank at the altar of Public Good, they'd have to sacrifice themselves and their careers, their hopes of ever being elected again, if they wanted to run a major bank effectively.

This reason completely trumps the sort of 'national pride' that he gives as #4; although I agree that there is a degree of Ango-Saxon capitalist pride that cries out against nationalizing anything, the elites in both the U.K. and U.S. are not the sorts to let anything as old-fashioned as pride or ideals or ethics to stand in the way of practical business. There's just no political will to do it: the last thing Congress wants to do is add "running a bank" to its list of troubles. (Given the fact that many of them are lawyers by profession in addition to being politicians, a bank nationalization would put them in line for the people-the-public-loves-to-hate trifecta.)

There are a couple of things here and there that I don't quite agree with, or perhaps just don't understand:

The trigger would be a general view in the markets that the government’s tax receipts weren’t sufficient to meet its debt payments. That would cause a ‘buyer’s strike’ in the bond market: nobody would want to buy UK government bonds, so the government could no longer keep going back to the markets for cash to pay its liabilities. That would leave the government facing an immediate need for cash with no means of raising it – and it’s that which would send us prostrate to the IMF.Why would Britain, in that instance, go to the IMF? Wouldn't they just do as the U.S. is doing right now, and monetize their debt? Issue new pounds sterling and immediately turn around and use them to buy government bonds, essentially short-cutting the public issuance process. It would drive up inflation like crazy, and personally I think it's probably worse in the long run, but it seems more politically feasible. Inflation goes up, everyone suffers, but nobody in power has to actually admit failure or go, hat in hand, to the IMF.

Does Britain have a prohibition against debt monetization that the U.S. does not? And if it does, is it realistic to expect that prohibition to remain in place in such a scenario? I'm skeptical.

posted by Kadin2048 at 3:06 PM on May 26, 2009 [2 favorites]

Let's say the value of the house drops to £100,000. What is your net equity now? The same? Even though you've still got the £200,000 mortgage?

Actually you don't mark fixed assets to market - but that's besides the point. The fact is the balance sheet is incorrect. There at 220k in assets, 140k in liabilities and 80k in equity. So actually even in your hypothetical you'd still be solvent.

But that would also be a lame argument to attack the piece with. Its actually quite well done and something I would suggest to people as a good starting off point - even if I vehemently disagree with his conclusions. The LRB's coverage of this mess has been absolutely fantastic.

On the list of ironies - people who for years rightfully derided market based solutions as being rife with conflicts and inefficiencies are now keen to embrace market values for distressed assets since those support their own schadenfreude at the collapse of the finance industry.

posted by JPD at 3:06 PM on May 26, 2009 [1 favorite]

Actually you don't mark fixed assets to market - but that's besides the point. The fact is the balance sheet is incorrect. There at 220k in assets, 140k in liabilities and 80k in equity. So actually even in your hypothetical you'd still be solvent.

But that would also be a lame argument to attack the piece with. Its actually quite well done and something I would suggest to people as a good starting off point - even if I vehemently disagree with his conclusions. The LRB's coverage of this mess has been absolutely fantastic.

On the list of ironies - people who for years rightfully derided market based solutions as being rife with conflicts and inefficiencies are now keen to embrace market values for distressed assets since those support their own schadenfreude at the collapse of the finance industry.

posted by JPD at 3:06 PM on May 26, 2009 [1 favorite]

"... Because nobody is spending money, even relatively blameless countries such as Germany, with low levels of debt and workforces who actually make things, are having a difficult time. Germany’s economy is predicted to contract by 5.4 per cent this year. A banker explained it like this: ‘When your country’s economy depends on people buying a car every three years, and they decide that they’ll only buy a car every five years, you’re fucked. Off a cliff.’ So the German economy is fucked off a cliff. But it will recover, when people start buying cars again, and when it does, at least their underlying levels of debt are manageable. ..."No kidding. In many parts of Germany, the bill for this international financial clusterf*sk is already coming due on school kids. Why should British and American school kids expect an easier future?

Ibid

posted by paulsc at 3:25 PM on May 26, 2009

It reads like a very long mefi comment.

posted by surrendering monkey at 3:52 PM on May 26, 2009 [1 favorite]

posted by surrendering monkey at 3:52 PM on May 26, 2009 [1 favorite]

Mutant, while i agree that sterling is/was oversold, I doubt that the inflows caused by real estate attractiveness can make up for the dwindling north sea petroleum income -- and sterling has already appreciated over 10% against EUR. Cant say that the BOE looks hawkish either -- and i guess financial services wont be growing much for a while. I'd rather have kronas or aussies,..

posted by 3mendo at 4:18 PM on May 26, 2009

posted by 3mendo at 4:18 PM on May 26, 2009

‘RBS is a responsible company. We carry out rigorous research so that we can be confident we know the issues that are most important to our stakeholders and we take practical steps to respond to what they tell us. Then occasionally, we blow all that shit off, fire up some crystal meth, and throw money around with such crazed abandon that it helps destroy the public finances of the world’s fifth biggest economy.’ See if you can guess which of those sentences is not in the [RBS corporate] report.

priceless.

posted by UbuRoivas at 4:32 PM on May 26, 2009

priceless.

posted by UbuRoivas at 4:32 PM on May 26, 2009

It reads like a very long mefi comment.

Wait, this Lanchester bloke was Ethereal Bligh?!??

posted by UbuRoivas at 5:19 PM on May 26, 2009

Wait, this Lanchester bloke was Ethereal Bligh?!??

posted by UbuRoivas at 5:19 PM on May 26, 2009

Wait, this Lanchester bloke was Ethereal Bligh?!??

Either that or it's a y2karl FPP.

posted by greycap at 11:12 PM on May 26, 2009

Either that or it's a y2karl FPP.

posted by greycap at 11:12 PM on May 26, 2009

Hey now... there's not a single blockquote anywhere!

mostly that's because I couldn't decide on any single passage to use, but still...

posted by Kattullus at 4:12 AM on May 27, 2009

mostly that's because I couldn't decide on any single passage to use, but still...

posted by Kattullus at 4:12 AM on May 27, 2009

Brilliant. Very readable and a great introduction to why everything's messed up. We're in a financial world war! Against... ourselves? The financial status quo? Hmm...

Also, he used the word synecdoche in context.

posted by Magnakai at 4:47 AM on May 27, 2009

Also, he used the word synecdoche in context.

posted by Magnakai at 4:47 AM on May 27, 2009

As usual, a brilliant article by John lancaster. Thanks for posting

posted by criticalbill at 6:19 AM on May 27, 2009

posted by criticalbill at 6:19 AM on May 27, 2009

synecdoche should always - by definition - be in context.

posted by UbuRoivas at 7:07 AM on May 27, 2009

posted by UbuRoivas at 7:07 AM on May 27, 2009

Needs more money.

posted by a non e mouse at 9:51 PM on May 27, 2009

posted by a non e mouse at 9:51 PM on May 27, 2009

Anyone feeling that John Lanchester perhaps wasn't thorough enough should consider reading the New Yorker's fourteen-page Nick Paumgarten essay: The Death of Kings (abstract only, payment req for full piece)

Incidentally in the latest new yorker is yet more from JL

posted by criticalbill at 5:04 AM on May 28, 2009

Incidentally in the latest new yorker is yet more from JL

posted by criticalbill at 5:04 AM on May 28, 2009

« Older The machines are making such a wonderful music... | Cry havoc and let loose the Dogs of War. Newer »

This thread has been archived and is closed to new comments

posted by Elmore at 1:29 PM on May 26, 2009