A Handout Is The Best Hand Up

November 9, 2015 3:46 PM Subscribe

A generation of evidence affirms cash transfers as among the most powerful means of eliminating extreme poverty in the world. Transfers of money, along with transfers of food vouchers, have seen Brazilian inequality plummet alongside the numbers of the very poor.

The fact is rich people, relative to poor people, don't spend money. The economy's engine of the world is fueled by the constant exchange of currency and rich people hoarding is an impediment to that happening.

posted by Talez at 4:32 PM on November 9, 2015 [44 favorites]

posted by Talez at 4:32 PM on November 9, 2015 [44 favorites]

Of note, if anyone is interested in philanthropy (i sometimes am), the group GiveDirectly follows the unconditional cash transfer model. I think i am biased to like them eve more given the fact that they are heavily data-driven, and have pretty graphics to prove their performance rather than pity photos.

posted by givesacrap at 4:37 PM on November 9, 2015 [24 favorites]

posted by givesacrap at 4:37 PM on November 9, 2015 [24 favorites]

Talez, how do you think banks and stocks work, or do you think millionaires keep their money in mattresses?

posted by michaelh at 4:38 PM on November 9, 2015 [6 favorites]

posted by michaelh at 4:38 PM on November 9, 2015 [6 favorites]

Sure the stored money of rich people circulates. It circulates to investments that enrich rich people.

posted by zippy at 4:54 PM on November 9, 2015 [16 favorites]

posted by zippy at 4:54 PM on November 9, 2015 [16 favorites]

Like my home loan, my dad's employer that pays him fairly, my mom's library's bond offering, etc. These investments pay a return, but they are definitely used by regular people. And when stocks are sold or a loan principal is returned, the cash is immediately reinvested or withdrawn to be spent.

posted by michaelh at 5:06 PM on November 9, 2015 [2 favorites]

posted by michaelh at 5:06 PM on November 9, 2015 [2 favorites]

The fact is rich people, relative to poor people, don't spend money. The economy's engine of the world is fueled by the constant exchange of currency and rich people hoarding is an impediment to that happening.

This isn't right, as mentioned earlier, rich people don't keep money under their mattress...

Some of their money might be in a savings account in the bank, which the bank uses to lend out to businesses or people who need a mortgage, who then pass the money onto the builders and contractors. It's not only rich people who need mortgages or work in construction.

Some of their money might be in stocks, which provides cash to the business allowing them to expand their operations. Again it's not only rich people who work in supermarkets or shop in them.

Money is pretty much always in circulation in the economy - it's not the circulation of it that's the issue. The scenario you're describing, where a "rich" person gets paid in cash and then keeps it in a safe in this basement - is pretty much only going to happen to a member of the mafia...

I recently visited a relatively poorer country and we tipped our guide the equivalent of nearly a full month's wages. Maybe I'd consider that a kind of direct cash transfer charity...

posted by xdvesper at 5:29 PM on November 9, 2015 [6 favorites]

This isn't right, as mentioned earlier, rich people don't keep money under their mattress...

Some of their money might be in a savings account in the bank, which the bank uses to lend out to businesses or people who need a mortgage, who then pass the money onto the builders and contractors. It's not only rich people who need mortgages or work in construction.

Some of their money might be in stocks, which provides cash to the business allowing them to expand their operations. Again it's not only rich people who work in supermarkets or shop in them.

Money is pretty much always in circulation in the economy - it's not the circulation of it that's the issue. The scenario you're describing, where a "rich" person gets paid in cash and then keeps it in a safe in this basement - is pretty much only going to happen to a member of the mafia...

I recently visited a relatively poorer country and we tipped our guide the equivalent of nearly a full month's wages. Maybe I'd consider that a kind of direct cash transfer charity...

posted by xdvesper at 5:29 PM on November 9, 2015 [6 favorites]

Go figure. Give a poor person money and they tend to stop being poor. Now if we could just get over the idea that nobody should be able to eat unless they've lined someone else's pockets for the requisite period (to be determined by the owner of said pockets), we'd be cooking with Crisco.

posted by Mooski at 5:35 PM on November 9, 2015 [5 favorites]

posted by Mooski at 5:35 PM on November 9, 2015 [5 favorites]

Like Zippy said, I think talez is talking about wealthy people hoarding capital, not cash. Money can circulate until the cows come home without ownership of the money being transferred to anyone. That's generally how rich people make money, if I'm not mistaken: they take the capital they have and they invest it in things that make interest, without giving up possession of the capital. Obviously rich people don't hoard cash. Brazil isn't lending money to poor people, it's giving it to them, that's the difference.

posted by Dr. Send at 5:40 PM on November 9, 2015 [24 favorites]

posted by Dr. Send at 5:40 PM on November 9, 2015 [24 favorites]

What is interesting is that rising labour income accounted for 3x the reduction in income inequality that these payments did. But apparently there was a resource-based labour boom that may have accounted for this, although you would think people not being desperate to take whatever job came by would have an effect as well.

posted by any portmanteau in a storm at 5:45 PM on November 9, 2015

posted by any portmanteau in a storm at 5:45 PM on November 9, 2015

Pretty much. Look at Apple for instance. $203b cash on hand. It's kept in things like T-notes and commercial paper. $600ish per capita is literally locked up in the business equivalent of a Scrooge McDuckian vault. If that was spread out to the entire United States we'd see economic stimulus like we've never seen before. But instead capital is hoarded for... reasons I guess. Tax avoidance mostly.

posted by Talez at 5:47 PM on November 9, 2015 [11 favorites]

posted by Talez at 5:47 PM on November 9, 2015 [11 favorites]

Talez: when you buy T-notes, you are (indirectly) lending the government money, which it then spends on running the government; when you buy "commercial paper," you are (indirectly) lending to other businesses.

Apple's $203b doesn't sit in a vault. What it means for Apple to have that money is that it retains the ability to pull it out and spend it on other (maybe less reversible) things if it so chooses.

Yes, Apple has a shitload of money that should probably be taxed or otherwise redistributed. But it just isn't true that the money isn't circulating.

posted by andrewpcone at 5:56 PM on November 9, 2015 [5 favorites]

Apple's $203b doesn't sit in a vault. What it means for Apple to have that money is that it retains the ability to pull it out and spend it on other (maybe less reversible) things if it so chooses.

Yes, Apple has a shitload of money that should probably be taxed or otherwise redistributed. But it just isn't true that the money isn't circulating.

posted by andrewpcone at 5:56 PM on November 9, 2015 [5 favorites]

michaelh: "Talez, how do you think banks and stocks work, or do you think millionaires keep their money in mattresses?"

"Banks and stocks", as you say, were not created, designed, or intended to address humanitarian concerns. In theoretical models, they can serve that purpose by making it easier for money to get from people who have it and want more, to those who don't and can offer something useful.

So right off the bat, they are completely unsuited to two major economic scenarios:

You're correct that millionaires don't literally keep their money in mattresses. Instead, they (figuratively) keep most of their money in slightly leaky waterbeds, and spend a lot of money on waterbed repair. If you're in the waterbed repair business (i.e. politics or finance), bully for you. Otherwise you'd better have a very efficient mechanism for filling your own waterbed from the lea... oh I give up.

Turns out bedroom furniture is way too reductive as a metaphor for economics, let alone economics as it relates to quality of life. Suffice it to say that extraordinary claims require extraordinary evidence, and those who make great claims about the benefits of our current financial system seem not-so-strong about and not-so-interested in the evidence.

More and more people are going to fall into group #2 above: the number of things that are most efficiently done by a human is dwindling incredibly rapidly. I'm a programmer, which some consider an automation-proof career... but in practice, I use Java and web technologies: tools and frameworks that automate the programmer equivalents to "manual labor" (assembly language, memory management, visual layout, network protocols). Even the priests of the financial system are threatened: high-frequency trading (while terrifying, given how easily a bug can get out of hand) can effect nimble and robust financial management that a human can never offer.

Something is going to happen to change how we think about wealth. It may be a return to serfdom and us thinking about money as something the rich have, and the rest of us might only achieve through extreme sacrifice and extreme luck. I hope it's something a bit more nuanced; it'll be a bummer if hundreds of years of economics, philosophy, and technology bring us right back to the feudal ages.

But if it's anything else, the closest analogue our current economic system seems to offer is to just give poor people cash. Give everyone cash if that's how you need to sell it, but the poor need cash and they need it now and (though this shouldn't be an ethical prerequisite) it benefits everyone if they have it.

posted by Riki tiki at 5:59 PM on November 9, 2015 [53 favorites]

"Banks and stocks", as you say, were not created, designed, or intended to address humanitarian concerns. In theoretical models, they can serve that purpose by making it easier for money to get from people who have it and want more, to those who don't and can offer something useful.

So right off the bat, they are completely unsuited to two major economic scenarios:

- People who have money and whose interest in increasing it is (proportionate to their wealth) below average, and

- People who need money, but have little to offer by the market's labor standards.

You're correct that millionaires don't literally keep their money in mattresses. Instead, they (figuratively) keep most of their money in slightly leaky waterbeds, and spend a lot of money on waterbed repair. If you're in the waterbed repair business (i.e. politics or finance), bully for you. Otherwise you'd better have a very efficient mechanism for filling your own waterbed from the lea... oh I give up.

Turns out bedroom furniture is way too reductive as a metaphor for economics, let alone economics as it relates to quality of life. Suffice it to say that extraordinary claims require extraordinary evidence, and those who make great claims about the benefits of our current financial system seem not-so-strong about and not-so-interested in the evidence.

More and more people are going to fall into group #2 above: the number of things that are most efficiently done by a human is dwindling incredibly rapidly. I'm a programmer, which some consider an automation-proof career... but in practice, I use Java and web technologies: tools and frameworks that automate the programmer equivalents to "manual labor" (assembly language, memory management, visual layout, network protocols). Even the priests of the financial system are threatened: high-frequency trading (while terrifying, given how easily a bug can get out of hand) can effect nimble and robust financial management that a human can never offer.

Something is going to happen to change how we think about wealth. It may be a return to serfdom and us thinking about money as something the rich have, and the rest of us might only achieve through extreme sacrifice and extreme luck. I hope it's something a bit more nuanced; it'll be a bummer if hundreds of years of economics, philosophy, and technology bring us right back to the feudal ages.

But if it's anything else, the closest analogue our current economic system seems to offer is to just give poor people cash. Give everyone cash if that's how you need to sell it, but the poor need cash and they need it now and (though this shouldn't be an ethical prerequisite) it benefits everyone if they have it.

posted by Riki tiki at 5:59 PM on November 9, 2015 [53 favorites]

I'm glad Riki tiki came along, because my only offhand response to the "Squaaaawk, banks and stocks, banks and stocks!" line that gets parroted every time someone accuses the rich people of hoarding (which that they do is patently obvious to everyone who isn't being disingenuous) is that it sounds pretty much like Econ 101 thinking, which means it's almost certainly bullshit hiding under a veneer of sensible-sounding verbiage. When a poor(er) person spends their money, the person to whom they give it doesn't have to worry about making payments and returning it with interest.

posted by Steely-eyed Missile Man at 6:41 PM on November 9, 2015 [14 favorites]

posted by Steely-eyed Missile Man at 6:41 PM on November 9, 2015 [14 favorites]

so, first I steal everything from you so that you are destitute. then, i give enough of it back so you can buy yourself a sandwich. Hooray! I've solved your extreme poverty!

Now, if only the richest thieves in the world would donate some of their loot so every starving person could buy a sandwich. that would be a real solution to world poverty.

posted by ennui.bz at 7:03 PM on November 9, 2015 [2 favorites]

Now, if only the richest thieves in the world would donate some of their loot so every starving person could buy a sandwich. that would be a real solution to world poverty.

posted by ennui.bz at 7:03 PM on November 9, 2015 [2 favorites]

ctrl-f "marginal utility"...

Quite simply, if I give the guy at the interstate off-ramp a fiver, he's gonna spend it. And the liquor store owner is gonna spend it again. Etc.

If I give my haughty, rich uncle a fiver...first he's gonna be like "I don't need charity from youuuu" and then he's gonna put it in his change drawer or whatever.

The next dollar has infinite utility to the guy that's broke. It has infinitesimal utility for the guy who's already got a bunch. That's why credits to the bottom 20% are so much better at stimulating the economy than tax cuts for the rich. And that's why this works so goddamn well.

posted by notsnot at 7:06 PM on November 9, 2015 [27 favorites]

Quite simply, if I give the guy at the interstate off-ramp a fiver, he's gonna spend it. And the liquor store owner is gonna spend it again. Etc.

If I give my haughty, rich uncle a fiver...first he's gonna be like "I don't need charity from youuuu" and then he's gonna put it in his change drawer or whatever.

The next dollar has infinite utility to the guy that's broke. It has infinitesimal utility for the guy who's already got a bunch. That's why credits to the bottom 20% are so much better at stimulating the economy than tax cuts for the rich. And that's why this works so goddamn well.

posted by notsnot at 7:06 PM on November 9, 2015 [27 favorites]

Yeah, it looks to me like the "money can't be hoarded" line of reasoning strongly implies that nobody actually has any money at all. I mean, you can characterize cash in the mattress as an interest-free loan to the United States, and everybody knows that the government spends money loaned to it on running the government, but of course the people the government pays to keep the government running either keep the money in bank accounts, stocks, or under their mattresses, and everyone knows that none of those things are real money for the reasons described by commenters above.

It's nonsense all the way down.

posted by burden at 7:26 PM on November 9, 2015

It's nonsense all the way down.

posted by burden at 7:26 PM on November 9, 2015

The fact is rich people, relative to poor people, don't spend money. The economy's engine of the world is fueled by the constant exchange of currency and rich people hoarding is an impediment to that happening."

The only way this is actually a problem is if you imagine rich people as Scrooge McDuck, literally swimming in the cash they hoard.

posted by pwnguin at 7:31 PM on November 9, 2015

The only way this is actually a problem is if you imagine rich people as Scrooge McDuck, literally swimming in the cash they hoard.

posted by pwnguin at 7:31 PM on November 9, 2015

Loaning money is not the same as spending it. Loaning it means there has to be a return. For example Apple's T-bills have to be paid back through a)taxes or b)more T-bills. All they do is defer the taxes until later. Now this is very useful - if you can use that money now to create economic growth greater than the percent you're going to pay for the return on investment to the holder of the bill. But in the long term, the value doesn't leave the hands of the organization with lots o' money.

if I spend $100 on something, whoever I bought from can spend it on whatever. If I invest $100, that person has to figure out how to make that more than $100 pretty quick. And if few people who want to buy stuff has non-loaned money, finding a something to sell and make a profit on becomes a lot harder. I mean sure that person can loan the money to yet a third person, but it can't be turtles all the way down - in the end someone has to be buying something or all this shuffling money about hasn't actually created any wealth.

posted by Zalzidrax at 7:49 PM on November 9, 2015 [3 favorites]

if I spend $100 on something, whoever I bought from can spend it on whatever. If I invest $100, that person has to figure out how to make that more than $100 pretty quick. And if few people who want to buy stuff has non-loaned money, finding a something to sell and make a profit on becomes a lot harder. I mean sure that person can loan the money to yet a third person, but it can't be turtles all the way down - in the end someone has to be buying something or all this shuffling money about hasn't actually created any wealth.

posted by Zalzidrax at 7:49 PM on November 9, 2015 [3 favorites]

Okay, I admit that mine was a kneejerk response, even if I think it was a silly throwaway comment that was later double downed in thread. But lets end the "how can you borrow money, pay it back and still make a profit" derail, and talk about the article. It appears cash transfers weren't responsible for the bulk of change:

posted by pwnguin at 7:59 PM on November 9, 2015

But if Bolsa Familia only accounted for 15 to 20 percent of the drop in income inequality in Brazil, what contributed the most? The same two studies agree that rising wages among the poor were the main driver of the decline in inequality in Brazil. While their methodologies differ slightly, the studies show that changes in labor income accounted for 55 to 60 percent of the drop in income inequality.Two years is a pretty huge shift when you consider that you can only feasibly accomplish that by retiring people and newly minted adults. If anything, Bolsa Familia appears to have been the carrot used to keep kids in school instead of working the fields.

And why did wages for the poor rise? Even before Bolsa Familia, the Brazilian government adopted policies that expanded access to education: Between 1995 and 2005, the average schooling among workers increased by almost two years. At the same time, the hourly wages for a worker with a given level of education rose much faster among the poor than the rest of the population, likely due to the increased demand for low-skilled labor that accompanied the commodity and price booms

posted by pwnguin at 7:59 PM on November 9, 2015

how many of you live in households taking home more than $100k per year? congrats! you are in the top 25% in the US by income.

you are rich. if you want to transfer income to the poor, it takes more than Scrooge McDuck.

posted by ennui.bz at 8:03 PM on November 9, 2015 [3 favorites]

you are rich. if you want to transfer income to the poor, it takes more than Scrooge McDuck.

posted by ennui.bz at 8:03 PM on November 9, 2015 [3 favorites]

For example Apple's T-bills have to be paid back through a)taxes or b)more T-bills. All they do is defer the taxes until later. Now this is very useful - if you can use that money now to create economic growth greater than the percent you're going to pay for the return on investment to the holder of the bill. But in the long term, the value doesn't leave the hands of the organization with lots o' money.

It doesn't leave their hands. It's used as leverage, you just said it yourself. The borrower creates multiples of the value of the money lent to them and keeps it for themself. And T-bills and commercial paper are paying less than inflation right now; inflation is redistributing their wealth whether they want it to or not.

posted by indubitable at 8:05 PM on November 9, 2015 [1 favorite]

It doesn't leave their hands. It's used as leverage, you just said it yourself. The borrower creates multiples of the value of the money lent to them and keeps it for themself. And T-bills and commercial paper are paying less than inflation right now; inflation is redistributing their wealth whether they want it to or not.

posted by indubitable at 8:05 PM on November 9, 2015 [1 favorite]

The problem is the upper middle class have the highest tax burden by percentage. I look at Romney's 12% and get fucking pissed because that's less than us. He's just an asshole with enough wealth to make sure he pays long term capital gains on everything he makes and deducts every fucking dollar he's ever lost.

posted by Talez at 8:07 PM on November 9, 2015 [1 favorite]

posted by Talez at 8:07 PM on November 9, 2015 [1 favorite]

But if it's anything else, the closest analogue our current economic system seems to offer is to just give poor people cash. Give everyone cash if that's how you need to sell it, but the poor need cash and they need it now and (though this shouldn't be an ethical prerequisite) it benefits everyone if they have it.

Sure. I made the statement earlier that rich people's money continue to circulate in the economy just like everyone else's, but this statement here is also probably true. It's hard to argue against redistribution of income. I'd like to point out the case of Australia - in Australia we give a surprising amount of cash directly to the poor as welfare - of the total 2010 Australian federal expenditure of about $300 billion, we gave out $76 billion as cash - no strings attached. (I picked 2010 because detailed data was published by the government in that year, a deep study is typically done every 5-10 years or so)

For that calendar year, there were 7.9 million full time workers in Australia, supporting a total of 6.1 million cash welfare recipients. Average cash handout was $12k per recipient per year - it's intended to be a 100% livable income, especially when paired with public housing programs. In some neighbourhoods, like the one adjacent to mine, around 30% of available units are public housing, where rent is capped at 25% of your income. This level of support may, or may not be sustainable - I pay effectively 40% marginal income tax and I'm only halfway to the top tax bracket.

For reference I made a large infographic covering and breaking down direct cash handouts in Australia based on the 2010 data.

posted by xdvesper at 9:06 PM on November 9, 2015 [1 favorite]

Sure. I made the statement earlier that rich people's money continue to circulate in the economy just like everyone else's, but this statement here is also probably true. It's hard to argue against redistribution of income. I'd like to point out the case of Australia - in Australia we give a surprising amount of cash directly to the poor as welfare - of the total 2010 Australian federal expenditure of about $300 billion, we gave out $76 billion as cash - no strings attached. (I picked 2010 because detailed data was published by the government in that year, a deep study is typically done every 5-10 years or so)

For that calendar year, there were 7.9 million full time workers in Australia, supporting a total of 6.1 million cash welfare recipients. Average cash handout was $12k per recipient per year - it's intended to be a 100% livable income, especially when paired with public housing programs. In some neighbourhoods, like the one adjacent to mine, around 30% of available units are public housing, where rent is capped at 25% of your income. This level of support may, or may not be sustainable - I pay effectively 40% marginal income tax and I'm only halfway to the top tax bracket.

For reference I made a large infographic covering and breaking down direct cash handouts in Australia based on the 2010 data.

{kind=link}

posted by xdvesper at 9:06 PM on November 9, 2015 [1 favorite]

Some of their money might be in a savings account in the bank, which the bank uses to lend out to businesses or people who need a mortgage, who then pass the money onto the builders and contractors. It's not only rich people who need mortgages or work in construction.

Minor nitpick: banks don't lend savings. Loans create deposits (pdf). And companies and (very rich) individuals are absolutely hoarding cash.

This seems to be be pretty much what Piketty's Capital was all about. Invested capital (i.e. wealth) grows faster than income and the only real notable period where this did not happen was the multi-decade period after WWII, which featured strong governmental intervention and redistribution of wealth. Some of the arguments here seem to be veering pretty close into trickle-down territory (which we now know to be garbage).

posted by triggerfinger at 9:14 PM on November 9, 2015 [7 favorites]

Minor nitpick: banks don't lend savings. Loans create deposits (pdf). And companies and (very rich) individuals are absolutely hoarding cash.

This seems to be be pretty much what Piketty's Capital was all about. Invested capital (i.e. wealth) grows faster than income and the only real notable period where this did not happen was the multi-decade period after WWII, which featured strong governmental intervention and redistribution of wealth. Some of the arguments here seem to be veering pretty close into trickle-down territory (which we now know to be garbage).

posted by triggerfinger at 9:14 PM on November 9, 2015 [7 favorites]

We are all interpreting Talez' original comment in our own way, even Talez.

I think he means that the vast majority of people basically spend what they earn. The very rich create surplus money and relative to everyone else, spend a very low percentage of it, a negative percentage actually for most.

If the rich were required to spend their money using the current system, the yacht industry might boom (although not as much as the how to hide your money industry) but that would create an economy based on the whims of a very small group, with corrosive effects on democracy.

To avoid these negative effects, instead of spending the money, it should just be put into a pool, and given to everyone else. Then those people can spend the money and amplify the existing economy.

posted by chaz at 9:52 PM on November 9, 2015 [1 favorite]

I think he means that the vast majority of people basically spend what they earn. The very rich create surplus money and relative to everyone else, spend a very low percentage of it, a negative percentage actually for most.

If the rich were required to spend their money using the current system, the yacht industry might boom (although not as much as the how to hide your money industry) but that would create an economy based on the whims of a very small group, with corrosive effects on democracy.

To avoid these negative effects, instead of spending the money, it should just be put into a pool, and given to everyone else. Then those people can spend the money and amplify the existing economy.

posted by chaz at 9:52 PM on November 9, 2015 [1 favorite]

that would create an economy based on the whims of a very small group, with corrosive effects on democracy

I guess the horses are about in the next county by now. Think I ought to close this barn door?

posted by Steely-eyed Missile Man at 9:59 PM on November 9, 2015 [3 favorites]

I guess the horses are about in the next county by now. Think I ought to close this barn door?

posted by Steely-eyed Missile Man at 9:59 PM on November 9, 2015 [3 favorites]

In other news, feeding hungry people makes them less hungry, and pouring water on dry people makes them wet.

I know, I'm being flippant again. But it's always nice to have the math to back up claims that seem to be self-evident. Yay math!

posted by stavrosthewonderchicken at 12:28 AM on November 10, 2015

I know, I'm being flippant again. But it's always nice to have the math to back up claims that seem to be self-evident. Yay math!

posted by stavrosthewonderchicken at 12:28 AM on November 10, 2015

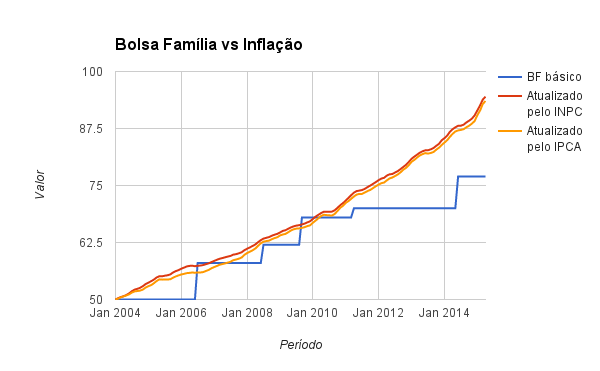

Bolsa Família is wonderful, but let's not forget that its success depended on a strong economy. A big discussion in Brazil right now is whether the current recession will nullify all the social progress from the past decades. In fact the number of people in extreme poverty has started growing again in 2013 (in Portuguese), and the increasing inflation has caught up with the cash transfer program.

Not that anyone is saying the current turmoil was caused by Bolsa Família, mind you. When the economy isn't doing great the poorest pay the heftiest price, and there's little cash transfer programs can do to change that.

posted by maskd at 1:14 AM on November 10, 2015 [1 favorite]

{kind=link}

Not that anyone is saying the current turmoil was caused by Bolsa Família, mind you. When the economy isn't doing great the poorest pay the heftiest price, and there's little cash transfer programs can do to change that.

posted by maskd at 1:14 AM on November 10, 2015 [1 favorite]

Thanks for the link to GiveDirectly it is fantastic.

I made an audible gasp of delight when I noticed that under each of their impressive stats button is a link entitled "Verify this" which links to a CVS of their data!

This is legit awesome. I am terrible at giving money to charity, because I am terrible at not spending all my money (though mostly it goes on outrageous nursery fees) but I am going to tweak my budget to send these folks some regular money, because a research driven proven highly effective charity which takes my rich person money and finds the poorest people and then just fucking gives it to them with no moralising or strings attached (apart from the rigorous verification and anti-corruption measures) is just the best.

posted by Just this guy, y'know at 3:57 AM on November 10, 2015 [4 favorites]

I made an audible gasp of delight when I noticed that under each of their impressive stats button is a link entitled "Verify this" which links to a CVS of their data!

This is legit awesome. I am terrible at giving money to charity, because I am terrible at not spending all my money (though mostly it goes on outrageous nursery fees) but I am going to tweak my budget to send these folks some regular money, because a research driven proven highly effective charity which takes my rich person money and finds the poorest people and then just fucking gives it to them with no moralising or strings attached (apart from the rigorous verification and anti-corruption measures) is just the best.

posted by Just this guy, y'know at 3:57 AM on November 10, 2015 [4 favorites]

Yet another conservative belief turns out to be false? You don't say.

posted by Gelatin at 7:05 AM on November 10, 2015 [2 favorites]

posted by Gelatin at 7:05 AM on November 10, 2015 [2 favorites]

Basically the problem is that this is all too complicated to talk about from macro level. The econ 101 stuff falls apart because rich people buying stocks is not the same as them spending money.

When they buy stocks, unless they're buying an IPO, the company doesn't get any of that money, it goes to the person selling the stock. The company got their money when they did their public offering. All they do now is figure out if they are better off reinvesting their profits into the company (hire people, build a factory, etc.) or return the equity to the stock holders in the form of a dividend and/or stock buy-back program. So stocks aren't great because it's just a way for investors to park some capital. It doesn't generate anymore buying or spending in the economy than the company was already spending. The only redeeming feature is that the seller now has some cash and is going to do something with it. Even if they're only buying more stock, someone at the end of that chain is cashing out some stock to actually spend it.

When mature companies need external funding, they usually get a loan from a bank or sell bonds. Both of these are helpful because the company is usually only going to issue debt like that to replace existing debt (which is basically just a placeholder for cash already circulating in the economy) or to fund some new capital expenditure (IE: Spending the money).

Banks work kind of the same way. A bunch of people park their money there to get both interest and convenient access (think about how much easier using a debit card to make internet purchases is than it would be to use mattress cash). Then they lend it out to people who are, almost always, going to immediately spend it on something. The problem here is that banks don't lend out every dollar they can. Sometimes they just have more deposits than they can lend, sometimes it regulatory or to mitigate risk. Or it can be a combination of all three.

What we're really talking about, in economic terms, the velocity of the money supply. Typically, a higher velocity will amplify the effects of economic stimulus more than a slower one. Stocks and bonds both slow down that velocity, but they don't stop it. Since the people who can't afford to invest their cash will pretty much always immediately spend every dollar, increased spending by that group has the greatest effect on the velocity. A simple solution is to tax gains on stocks and bonds and give that money to the poor. If done in the right amounts, everyone benefits. The poor person is less poor and has a better shot at moving up the socioeconomic ladder and the rich guy gets a better total return on his stock than he would otherwise.

Another way to look at it is that poor people tend to be a net draw on an economy. More tax dollars are spend on them then they generate and this is bad for government budgets (I don't really think it is but enough voters think so that it's basically true). So, what the government, as a representative of society, has is an investment opportunity. Odds are good that any specific poor person will have a few issues that keep them in a cycle of poverty. Things like free healthcare are great because you're going to save a bunch of money on unpaid hospital bills for some and others are going to be healthy enough to now get and hold a job/better job. Just that one thing will turn a bunch of poor citizens from tax sinks into tax generators. Healthcare is, I think, the lowest hanging fruit here but similar programs for education, transportation, infrastructure projects, even basic income schemes can be thought of in the same way. Invest in your least successful citizens and most of them will pay dividends.

If part of Ford's success was that they paid their workers enough to be able afford to buy the cars they made, I think that there is an argument that if wealth redistribution is done correctly, the wealth people still end up with more wealth than they started with.

posted by VTX at 10:14 AM on November 10, 2015 [6 favorites]

When they buy stocks, unless they're buying an IPO, the company doesn't get any of that money, it goes to the person selling the stock. The company got their money when they did their public offering. All they do now is figure out if they are better off reinvesting their profits into the company (hire people, build a factory, etc.) or return the equity to the stock holders in the form of a dividend and/or stock buy-back program. So stocks aren't great because it's just a way for investors to park some capital. It doesn't generate anymore buying or spending in the economy than the company was already spending. The only redeeming feature is that the seller now has some cash and is going to do something with it. Even if they're only buying more stock, someone at the end of that chain is cashing out some stock to actually spend it.

When mature companies need external funding, they usually get a loan from a bank or sell bonds. Both of these are helpful because the company is usually only going to issue debt like that to replace existing debt (which is basically just a placeholder for cash already circulating in the economy) or to fund some new capital expenditure (IE: Spending the money).

Banks work kind of the same way. A bunch of people park their money there to get both interest and convenient access (think about how much easier using a debit card to make internet purchases is than it would be to use mattress cash). Then they lend it out to people who are, almost always, going to immediately spend it on something. The problem here is that banks don't lend out every dollar they can. Sometimes they just have more deposits than they can lend, sometimes it regulatory or to mitigate risk. Or it can be a combination of all three.

What we're really talking about, in economic terms, the velocity of the money supply. Typically, a higher velocity will amplify the effects of economic stimulus more than a slower one. Stocks and bonds both slow down that velocity, but they don't stop it. Since the people who can't afford to invest their cash will pretty much always immediately spend every dollar, increased spending by that group has the greatest effect on the velocity. A simple solution is to tax gains on stocks and bonds and give that money to the poor. If done in the right amounts, everyone benefits. The poor person is less poor and has a better shot at moving up the socioeconomic ladder and the rich guy gets a better total return on his stock than he would otherwise.

Another way to look at it is that poor people tend to be a net draw on an economy. More tax dollars are spend on them then they generate and this is bad for government budgets (I don't really think it is but enough voters think so that it's basically true). So, what the government, as a representative of society, has is an investment opportunity. Odds are good that any specific poor person will have a few issues that keep them in a cycle of poverty. Things like free healthcare are great because you're going to save a bunch of money on unpaid hospital bills for some and others are going to be healthy enough to now get and hold a job/better job. Just that one thing will turn a bunch of poor citizens from tax sinks into tax generators. Healthcare is, I think, the lowest hanging fruit here but similar programs for education, transportation, infrastructure projects, even basic income schemes can be thought of in the same way. Invest in your least successful citizens and most of them will pay dividends.

If part of Ford's success was that they paid their workers enough to be able afford to buy the cars they made, I think that there is an argument that if wealth redistribution is done correctly, the wealth people still end up with more wealth than they started with.

posted by VTX at 10:14 AM on November 10, 2015 [6 favorites]

That reasoning works on a subset of wealthy people who truly see the world as an abundant place full of mutually beneficial transactions.

I think most super rich people do feel like the pie doesn't get ever bigger, it just gets cut into smaller pieces and damned if someone who didn't work hard enough is going to get an extra piece, even if the wealthy person stands to benefit. Put another way they would prefer to heavily rate limit upward mobility for fear of losing out to more competition. Once you let enough poor folks taste the pie they're going to demand even more and are going to compete against you directly. Give them free education and teach them that hard work is truly rewarded and suddenly everyone is morally righteous enough to be wealthy? Noes.

posted by aydeejones at 11:10 AM on November 10, 2015

I think most super rich people do feel like the pie doesn't get ever bigger, it just gets cut into smaller pieces and damned if someone who didn't work hard enough is going to get an extra piece, even if the wealthy person stands to benefit. Put another way they would prefer to heavily rate limit upward mobility for fear of losing out to more competition. Once you let enough poor folks taste the pie they're going to demand even more and are going to compete against you directly. Give them free education and teach them that hard work is truly rewarded and suddenly everyone is morally righteous enough to be wealthy? Noes.

posted by aydeejones at 11:10 AM on November 10, 2015

And of course Henry Ford was selling cars that have a solid tangible benefit to anyone who can afford one. Interest, on the other hand, is how most wealthy people earn a living and interest is only valuable when you have a constant stream of people who can't afford things like, well, cars and homes. The person who gets the "right" to be in debt has agreed to surrender more than the agreed upon value of something simply to have it now knowing they will have to work harder to pay it back. Typically the items in question are so expensive that the majority of the population has to get into debt to acquire them. Meanwhile the party providing the loan simply has to ensure that there is always demand for their product (interest) and the only way to make sure most people don't have enough money to avoid paying interest is to shake them down, constantly and control wages. The poorer you get the more shakedowns you get in the form of check cashing fees, payday loans etc. A large number of people must work harder and pay more for the same basic commodities of daily living to ensure that a small class of fabulously rich folks can earn a living selling artificial abundance, and must maintain artificial scarcity of the chief commodity, money itself, and by overworking the labor force and keeping the unemployment level dialed in to "just high enough" you can effectively play the middle class like a turntable

posted by aydeejones at 11:18 AM on November 10, 2015 [2 favorites]

posted by aydeejones at 11:18 AM on November 10, 2015 [2 favorites]

It's been lost that stocks were created for the non-elite. Capital costs could be spread out among a large number of people, rather than only the few wealthy enough to fund the entire investment.

Also lost is the role of government. It took hundreds of years to create a legal framework so that people weren't constantly swindled by corporations, because they were not beholden to their shareholders.

Those two things were absolutely critical to funding the industrial revolution.

Pooling and reallocating resources, with protections in place for participants, transformed our economy from subsistence to relative wealth. It isn't something that is out of step with capitalism and economics. It's just easily forgotten.

posted by politikitty at 12:28 PM on November 10, 2015 [4 favorites]

Also lost is the role of government. It took hundreds of years to create a legal framework so that people weren't constantly swindled by corporations, because they were not beholden to their shareholders.

Those two things were absolutely critical to funding the industrial revolution.

Pooling and reallocating resources, with protections in place for participants, transformed our economy from subsistence to relative wealth. It isn't something that is out of step with capitalism and economics. It's just easily forgotten.

posted by politikitty at 12:28 PM on November 10, 2015 [4 favorites]

Minor nitpick: banks don't lend savings. Loans create deposits (pdf).

Really interesting...

Correct me if I'm wrong - I wish there was an easier to read explanation than that PDF - anyone want to attempt one for me, I don't work in banking - My reading of it is that in aggregate, banks as a industry don't lend reserves (customer deposits) out when creating loans. This is because, if a bank makes a loan, 99% of the time, their individual reserve will fall, and the loan is usually not taken out in cash -> that money is transferred into another person's bank account, which becomes part of the overall banking industry reserve anyway. So total bank reserves remain the same, but one bank's reserve has gone down while another has gone up. Some transactions will happen with interbank transactions / feds in the background to make sure reserve requirements for individual banks are met.

The only way the aggregate bank reserves will fall when a new loan is made is if someone borrows a million dollars and then hides it under his mattress (which is never). In that case, then yes, the banking system "may" utilize additional savings deposits to increase its reserves to compensate, but even then it can also gain additional reserves by borrowing them from the central bank instead - at a higher rate than savings deposits. So they're substitutes, but customer savings deposits are preferred. Is there more complexity here - can savings rates be above BLR?

Otherwise if we took that statement at its face value (for individual banks there's no link between savings and lending) there could be a hypothetical (standalone) bank that only makes loans but does not take any deposits. A bank that borrows 100% of its reserves from the central bank, with no actual deposits from non government parties, and only lends money out?

I'm seeing the misconception of savings -> loans like the high school chemistry model of electrons orbiting a nucleus - a helpful visualization, but not strictly true.

posted by xdvesper at 2:56 PM on November 10, 2015

Really interesting...

Correct me if I'm wrong - I wish there was an easier to read explanation than that PDF - anyone want to attempt one for me, I don't work in banking - My reading of it is that in aggregate, banks as a industry don't lend reserves (customer deposits) out when creating loans. This is because, if a bank makes a loan, 99% of the time, their individual reserve will fall, and the loan is usually not taken out in cash -> that money is transferred into another person's bank account, which becomes part of the overall banking industry reserve anyway. So total bank reserves remain the same, but one bank's reserve has gone down while another has gone up. Some transactions will happen with interbank transactions / feds in the background to make sure reserve requirements for individual banks are met.

The only way the aggregate bank reserves will fall when a new loan is made is if someone borrows a million dollars and then hides it under his mattress (which is never). In that case, then yes, the banking system "may" utilize additional savings deposits to increase its reserves to compensate, but even then it can also gain additional reserves by borrowing them from the central bank instead - at a higher rate than savings deposits. So they're substitutes, but customer savings deposits are preferred. Is there more complexity here - can savings rates be above BLR?

Otherwise if we took that statement at its face value (for individual banks there's no link between savings and lending) there could be a hypothetical (standalone) bank that only makes loans but does not take any deposits. A bank that borrows 100% of its reserves from the central bank, with no actual deposits from non government parties, and only lends money out?

I'm seeing the misconception of savings -> loans like the high school chemistry model of electrons orbiting a nucleus - a helpful visualization, but not strictly true.

posted by xdvesper at 2:56 PM on November 10, 2015

interest is only valuable when you have a constant stream of people who can't afford things like, well, cars and homes.

So nearly every newly minted 18 year old, who is born short a home. Or publicly traded companies, who frequently issue corporate paper to finance factory expansions and other capital purchases. Or more nefariously, governments who wish to raise an army to fight the French and Spanish navies.

Interest is useful as a proxy for discount rate -- how much do we prefer money now versus later. Soviet plywood production planner and Nobel Laureate Kantorovich demonstrated that even centrally planned economies need something resembling price and interest rates to decide between production now and production later. I say proxy, because there are other things built into the rates, like inflation expectations, and risk.

To bring this back on the topic of relieving poverty in the developing world, the reality is that Brazillian overnight rates range between 7 and 20 percent. Much of that is inflation, as their currency inflation rate approaches 10 percent. Hence maskd's point that inflation is eroding the power of Bolsa Familia.

IMO, the interesting point of this program is not 'giving versus lending'. It is about how to give: are cash handouts are more effective than social services? The cash handout line goes "If you give people money, they know far better than a government worker how allocate it to what works best for them." The social services line goes something like "they'll just spend it on booze and televisions; we need conditions placed on cash transfers as additional self-control." Naturally, the problem is that economists cannot control for things like a long running commodities boom (and subsequent bust).

posted by pwnguin at 4:53 PM on November 10, 2015 [1 favorite]

So nearly every newly minted 18 year old, who is born short a home. Or publicly traded companies, who frequently issue corporate paper to finance factory expansions and other capital purchases. Or more nefariously, governments who wish to raise an army to fight the French and Spanish navies.

Interest is useful as a proxy for discount rate -- how much do we prefer money now versus later. Soviet plywood production planner and Nobel Laureate Kantorovich demonstrated that even centrally planned economies need something resembling price and interest rates to decide between production now and production later. I say proxy, because there are other things built into the rates, like inflation expectations, and risk.

To bring this back on the topic of relieving poverty in the developing world, the reality is that Brazillian overnight rates range between 7 and 20 percent. Much of that is inflation, as their currency inflation rate approaches 10 percent. Hence maskd's point that inflation is eroding the power of Bolsa Familia.

IMO, the interesting point of this program is not 'giving versus lending'. It is about how to give: are cash handouts are more effective than social services? The cash handout line goes "If you give people money, they know far better than a government worker how allocate it to what works best for them." The social services line goes something like "they'll just spend it on booze and televisions; we need conditions placed on cash transfers as additional self-control." Naturally, the problem is that economists cannot control for things like a long running commodities boom (and subsequent bust).

posted by pwnguin at 4:53 PM on November 10, 2015 [1 favorite]

The only way the aggregate bank reserves will fall when a new loan is made is if someone borrows a million dollars and then hides it under his mattress (which is never). In that case, then yes, the banking system "may" utilize additional savings deposits to increase its reserves to compensate, but even then it can also gain additional reserves by borrowing them from the central bank instead - at a higher rate than savings deposits.

Yes, reserves can (essentially) only leave the banking system by people withdrawing cash and not redepositing it. The Fed can also remove reserves from the system.

Banks can pretty much always meet any shortfall on their reserve requirements through the interbank lending market (borrowing from other banks), which is very short-term (overnight), at very low rates (currently 0.25%) and under which the money is available immediately. The Fed acts as a lender of last resort via the discount window at a slightly higher rate (0.75%).

Otherwise if we took that statement at its face value (for individual banks there's no link between savings and lending) there could be a hypothetical (standalone) bank that only makes loans but does not take any deposits. A bank that borrows 100% of its reserves from the central bank, with no actual deposits from non government parties, and only lends money out?

The thing that prevents this is the capital requirements imposed on banks, which have gotten stricter post-2008 (and which are different than reserve requirements).

This piece from Liberty Street Economics (the blog of the New York Fed) also has a great explanation on the banking system, especially as it relates to excess reserves.

posted by triggerfinger at 6:41 PM on November 10, 2015

Yes, reserves can (essentially) only leave the banking system by people withdrawing cash and not redepositing it. The Fed can also remove reserves from the system.

Banks can pretty much always meet any shortfall on their reserve requirements through the interbank lending market (borrowing from other banks), which is very short-term (overnight), at very low rates (currently 0.25%) and under which the money is available immediately. The Fed acts as a lender of last resort via the discount window at a slightly higher rate (0.75%).

Otherwise if we took that statement at its face value (for individual banks there's no link between savings and lending) there could be a hypothetical (standalone) bank that only makes loans but does not take any deposits. A bank that borrows 100% of its reserves from the central bank, with no actual deposits from non government parties, and only lends money out?

The thing that prevents this is the capital requirements imposed on banks, which have gotten stricter post-2008 (and which are different than reserve requirements).

This piece from Liberty Street Economics (the blog of the New York Fed) also has a great explanation on the banking system, especially as it relates to excess reserves.

posted by triggerfinger at 6:41 PM on November 10, 2015

Back in the 1980s, writer and anti-government-waste crusader Martin Gross calculated that for the cost the government was spending on literally innumerable overlapping and inefficient welfare programs, we could just cut an annual check for $30,000 (1980s money!) to every family of four under the poverty line -- and the result would be far, far more money actually in their pockets.

posted by Alaska Jack at 8:26 PM on November 10, 2015

posted by Alaska Jack at 8:26 PM on November 10, 2015

Meanwhile the party providing the loan simply has to ensure that there is always demand for their product (interest) and the only way to make sure most people don't have enough money to avoid paying interest is to shake them down, constantly and control wages...and keeping the unemployment level dialed in to "just high enough" you can effectively play the middle class like a turntable

I follow what you are saying here but it does not seem to follow reality. Based on historical data, interest rates are typically in the 1-4% range, except for the mid-70's to mid-90's when they jumped through the roof and then returned to low levels. Also, the increase in fees and other ways to charge customers for services that were previously free is a relatively new phenomenon (recent as in the last 15-20 years), which is a period of falling interest rates.

posted by LizBoBiz at 11:03 AM on November 11, 2015

I follow what you are saying here but it does not seem to follow reality. Based on historical data, interest rates are typically in the 1-4% range, except for the mid-70's to mid-90's when they jumped through the roof and then returned to low levels. Also, the increase in fees and other ways to charge customers for services that were previously free is a relatively new phenomenon (recent as in the last 15-20 years), which is a period of falling interest rates.

posted by LizBoBiz at 11:03 AM on November 11, 2015

Back in the 1980s, writer and anti-government-waste crusader Martin Gross calculated that for the cost the government was spending on literally innumerable overlapping and inefficient welfare programs, we could just cut an annual check for $30,000 (1980s money!) to every family of four under the poverty line -- and the result would be far, far more money actually in their pockets.

If we were to do that today the poverty rate is 14.8 percent. Assuming you took away all the money the government spends on social security, unemployment and welfare (1.2T) that gives you $30,000 for 4 million families give or take a hundred thousand.

That doesn't add up even considering how much less $30,000 is worth today.

posted by Talez at 4:39 PM on November 11, 2015

If we were to do that today the poverty rate is 14.8 percent. Assuming you took away all the money the government spends on social security, unemployment and welfare (1.2T) that gives you $30,000 for 4 million families give or take a hundred thousand.

That doesn't add up even considering how much less $30,000 is worth today.

posted by Talez at 4:39 PM on November 11, 2015

Assuming you took away all the money the government spends on social security, unemployment and welfare (1.2T)

To be fair, you're only looking at federal dollars, while I think the point is at the state level there is considerable duplication of effort when it comes to infrastructure. And AFDC had much more infrastructure than it's replacement TANF.

Not that paternalistic targeted programs are necessarily inferior to hard cash. Education is preferable to living expenses and hoping kids figure out enough to join the workforce. And it's easier to get the political will to create a paternalistic safety net than basic income. If only because we're a society of judgmental dicks

posted by politikitty at 5:21 PM on November 11, 2015

To be fair, you're only looking at federal dollars, while I think the point is at the state level there is considerable duplication of effort when it comes to infrastructure. And AFDC had much more infrastructure than it's replacement TANF.

Not that paternalistic targeted programs are necessarily inferior to hard cash. Education is preferable to living expenses and hoping kids figure out enough to join the workforce. And it's easier to get the political will to create a paternalistic safety net than basic income. If only because we're a society of judgmental dicks

posted by politikitty at 5:21 PM on November 11, 2015

Assuming you took away all the money the government spends on social security, unemployment

Why would you do that? Those are a pension plan and insurance, respectively. They are not welfare; people get out of the system what they pay into it.

posted by indubitable at 7:38 PM on November 11, 2015

Why would you do that? Those are a pension plan and insurance, respectively. They are not welfare; people get out of the system what they pay into it.

posted by indubitable at 7:38 PM on November 11, 2015

Because if there was a GBI the need for social security and unemployment insurance would significantly decrease. If you're already getting a check for $30,000 per year (which is more than the current SS average of about 14k) then you don't need social security.

We started those insurance programs to begin with because there was no safety net. GBI would be the new safety net and so those programs wouldn't be needed and could be rolled into the GBI.

posted by LizBoBiz at 5:53 AM on November 13, 2015

We started those insurance programs to begin with because there was no safety net. GBI would be the new safety net and so those programs wouldn't be needed and could be rolled into the GBI.

posted by LizBoBiz at 5:53 AM on November 13, 2015

Indeed, another way to think of such a program is Social Security For All. Unfortunately, Talez's math assumes differently. 1.2 trillion divided by the entire US population is 4 thousand. Even households is only 14k a year. Moreover, the US census describes 115 million households and a poverty rate of 15 percent, for 17 million families in poverty, not 4 million. To get to 30k in basic income per family, the US budget would need to be 3.45 trillion dollars, compared with last year's US expenditures of 3.5 trillion. This is quite the shift.

Probably the biggest concern I have with such a plan is the effects of a sudden shift in spending of that money. Every time my union wins a better contract, my landlord delivers a letter announcing that my rent went up by exactly the same percentage. Same principle applies on a broader scale: if we can't (or won't) immediately produce what will buy when granted the income, prices of inelastic goods will skyrocket.

posted by pwnguin at 9:14 AM on November 13, 2015

Probably the biggest concern I have with such a plan is the effects of a sudden shift in spending of that money. Every time my union wins a better contract, my landlord delivers a letter announcing that my rent went up by exactly the same percentage. Same principle applies on a broader scale: if we can't (or won't) immediately produce what will buy when granted the income, prices of inelastic goods will skyrocket.

posted by pwnguin at 9:14 AM on November 13, 2015

« Older Grave Metallum | I guess it’s sunglasses all the time now Newer »

This thread has been archived and is closed to new comments

posted by shadow vector at 4:21 PM on November 9, 2015 [69 favorites]