Platform Cooperatives: Money as a (Public) Service

February 11, 2016 12:34 AM Subscribe

In Sweden, a Cash-Free Future Nears - "Few places are tilting toward a cashless future as quickly as Sweden, which has become hooked on the convenience of paying by app and plastic."tolls rents fees from them, while central banks provide cash management services and real-time gross settlement for banks nearly free?*

Time for a digital government mint - "E-cash for the people: Phase out cash, phase in official digital money"

-The Digitization of Finance[1,2,3]

-The Future of Money

-Digital money, negative rates as Gosplan 2.0

-RTGS, and the story of batches instead of blocks

-RTGS, and the story of collateralised risk instead of credit risk

-Fintech: Search for a super-algo[1,2]

-Fintech paradoxes, blacklist edition[*]

-Scaling, and why unicorns can't survive without it

-On unicorn imperialism

-On the hypothetical eventuality of no more free internet

-The Rise of the Platform Economy

-Putting powerful platforms under cooperative control: "People gathered to talk about the problems of an online economy reliant on monopoly, extraction, and surveillance—and discuss how to build a cooperative Internet, built of platforms owned and governed by the people who rely on them." (This house proposes that we nationalise Uber)

So now onto (more hype about) Bitcoin/blockchains:

*Fedwire was free for members until 1981, effectively subsidizing commercial interests; that is, banks get all these services for next to nothing (at cost, but still at taxpayer expense), presumably to 'grease the wheels of capitalism', but if any of these services were offered to the public -- in the public interest (postal banking anyone?) -- it would be deemed 'socialist'. What does it say about capitalist institutions then that practice 'socialism for me, but not for thee'?

oh and fwiw, a quick detour/primer on 'what is money?':

Mr. Eriksson, who now heads the Association of Swedish Private Security Companies, a lobbying group for firms providing security for cash transfers, accuses banks and credit card companies of trying to “price cash out of the market” to make way for cards and electronic payments, which generate fee income.So forget about Bitcoin and blockchains for a moment. Why should private banks and credit card companies get to control payment systems and generate

Time for a digital government mint - "E-cash for the people: Phase out cash, phase in official digital money"

Two profound changes are under way in our attitudes towards money, both of which could in short order transform how most of us deal with the banking system, and indeed how the system itself works. The first trend is a growing preference for electronic means of payment over cash. The other is the growing push for central banks themselves to issue electronic money for use by individuals...Fedcoin—how banks can survive blockchains (via)

Wrapping one’s head around the difference between official versus private money is a lot harder than understanding the distinction between physical and electronic money — but it is also essential for making informed judgments about financial and monetary policy (we have previously explained why). Well done, therefore, to Positive Money, which has just published a report arguing how and why official digital currency should be introduced in the UK. The thoughtful and thorough report qualifies as essential reading.

The general idea is for the Bank of England (or other central banks; the ideas are general) to offer deposit accounts directly to the public, or alternatively, for private banks to offer accounts fully backed by central bank reserves. The authors go through the mechanics of how this would work, and address the main objections. We only discuss the most important of these here (but do read the whole report), which is that the system may work too well.

Too well, that is, in that people would convert a very large share of their current bank deposits into official digital money, in effect taking them out of the private banking system. Why might this be a problem? [P]eople may prefer the safety of central bank accounts even in normal times. That would destroy private banks’ current deposit-funded model. Is that a bad thing? They would still have a role as direct intermediators between savers and borrowers, by offering investment products sufficiently attractive for people to get out of the safety of e-cash. Meanwhile, the broad money supply would be more directly under the control of the central bank, whereas now it’s a product of the vagaries of private lending decisions. The more of the broad money supply that was in the form of official digital cash, the easier it would be, for example, for the central bank to use tools such as negative interest rates or helicopter drops. Both could be indispensable in the years ahead.

If the Fedcoin took off, it would appear to be the death knell for credit card providers and deposit-taking institutions. Banks would have two options to avoid economic obsolescence. The first would be to transition toward a pure investment banking strategy, financed entirely via equity and long-term debt raised from savers aware of the risk they were taking. Indeed, this is the model favoured by neo-classical economists harking back to the ideas of Irving Fisher.Are Banks Destined To Become The Next “Dumb Pipes”? (via)

A second option would be to attract Fedcoin deposits by providing services such as verification for know-your-customer and anti-money-laundering rules or secure digital wallets or even just the most user-friendly apps. Banks could compete for Fedcoin deposits by issuing their own blockchains, at par with Fedcoin. Deutsche Bank,[1,2] for example, could issue dbCoin, which customers use to settle transactions with any counterparty, much like a digital chequebook. Banks would guarantee convertibility of their digital currencies into Fedcoin, and central banks offer clearing and settlement facilities.

This brings us full circle back to today’s system, but with a couple of important exceptions. For starters, the difference between the monetary base and bank-created, branded money would be considerably clearer. More important, perhaps, the technological obsolescence of deposit-taking institutions engenders greater economic competitiveness. The banking sector would no longer be rewarded for processing payments or managing current accounts. It would have to compete for deposits by offering better services and ultimately greater responsibility for the money it creates.

{kind=link}

{kind=link}

The telcos hate the term “dumb pipes” — and for good reason. They are being relegated to the common conduits through which meaningful communications and commerce take place. But telcos won’t go away overnight because there’s still a lot of value in the physical network infrastructure and cell towers they built through decades of investment.Fiatcoin, redefining Banks and Banking (via)

Similarly, “unbundled” banks won’t go away overnight; there’s still a lot of value in the intra-bank money transfer networks and the depository role that banks are uniquely allowed to play in the U.S. economy. However, over time, traditional banks that fail to dramatically reinvent themselves for modern consumers will find themselves playing the role of a simple inbox for depository funds and pipes that move the money to other financial services providers who will increasingly influence consumers’ financial lives.

What of cross border transactions? Would various central banks use the same consensus technology stack with same or similar features (consensus algorithm, network topology, monetary policy scripting) thereby ensuring optimal interoperability? Would central banks introduce a tiered approach with a shared metafiatcoin only available and transacted amongst themselves (hello IMF and SDRs) linked to country or country unions' specific fiatcoins (fedcoin, eurocoin...)also btw...

Until fiatcoin would be made available to the public - and I am also convinced this will happen sooner than we think - how would financial institutions intermediate between fiatcoin and physical currencies (physical or digital cash)?

-The Digitization of Finance[1,2,3]

-The Future of Money

-Digital money, negative rates as Gosplan 2.0

-RTGS, and the story of batches instead of blocks

-RTGS, and the story of collateralised risk instead of credit risk

-Fintech: Search for a super-algo[1,2]

-Fintech paradoxes, blacklist edition[*]

-Scaling, and why unicorns can't survive without it

-On unicorn imperialism

-On the hypothetical eventuality of no more free internet

-The Rise of the Platform Economy

-Putting powerful platforms under cooperative control: "People gathered to talk about the problems of an online economy reliant on monopoly, extraction, and surveillance—and discuss how to build a cooperative Internet, built of platforms owned and governed by the people who rely on them." (This house proposes that we nationalise Uber)

So now onto (more hype about) Bitcoin/blockchains:

- The Plan to Unite Bitcoin With All Other Online Currencies - "The idea is to create a single worldwide network that can not only unite all digital currencies, but all companies and individuals who use those currencies."

- Linux Foundation Unites Industry Leaders to Advance Blockchain Technology - "The project will develop an enterprise grade, open source distributed ledger framework and free developers to focus on building robust, industry-specific applications, platforms and hardware systems to support business transactions." (via)

- The three pillars of a crypto-law ecosystem: Identity, Assets, Data - "Just as the GNU portion of GNU/Linux provides important pieces of software 'infrastructure' for a functional operating system (such as a C library and shell tools), the Ethereum platform, at present, needs this infrastructure before it can be properly exploited. This article is about mapping out and exploring the interrelationships between those pieces and doing so in terms of defining and (re)combining simple primitives."

- Blockchain Technology Predictions - "So while Ethereum — which is presently capable of 25 transaction per second (TPS) — is not in danger of bumping up against difficult scaling issues soon, it will be able to handle many TPS with Ethereum version 2.0, levels commensurate with what the Visa and American Express networks." (via)

- Blockchain hype storms Davos - "Banks know that forging a cartel as strong as that eliminates all possibility of out competing with each other in terms of risk, screening and security. As far as they're concerned, they become one bank (with all the non-diversity risk that comes with monopoly systems). It also means erroneous transactions become nigh impossible to reverse, money supply becomes a constant and scaling is compromised completely. Hence the rage for private blockchains with the promise to provide banks with override options within their special trusted network."

The hope is that the protocol will increase the adoption of online money and, more broadly, let us more efficiently send money from place to place. That’s the goal of many existing projects. Ripple and Stellar, for instance, are designed so that you can send any currency and have it arrive as any other currency. You can send bitcoin and have them arrive as litecoin. You can send good ol’ US dollars and have them arrive as dogecoin. The rub is that the community of businesses and developers who use these ledgers is limited—and you can’t send money from one network to another. The interledger protocol aims to change that.

In a way, the project is the apotheosis of a decades-long effort to create what you might call “an Internet for money.” Back in the early ’90s, people like Marc Andreessen, the creator of the Netscape web browser, hoped to create an standard way of sending money across the web. The original hypertext transfer protocol—http, the standard that defined the underpinnings of the web—actually included a code for payments. Though this was never used, many outfits in recent years have tried at least to create a de facto standard for online money...

*Fedwire was free for members until 1981, effectively subsidizing commercial interests; that is, banks get all these services for next to nothing (at cost, but still at taxpayer expense), presumably to 'grease the wheels of capitalism', but if any of these services were offered to the public -- in the public interest (postal banking anyone?) -- it would be deemed 'socialist'. What does it say about capitalist institutions then that practice 'socialism for me, but not for thee'?

oh and fwiw, a quick detour/primer on 'what is money?':

- What makes money special, the lawyer's edition - "Economists like to say that money is unique because it is a medium of exchange, store of value, and unit of account. Lawyers and judges have a different story to tell about money's uniqueness. Unlike goods, money can't be 'followed.' "[1,2,3,4,5]

- Money as a social construct and public good - "As long as we remain ignorant of how monetary systems operate, for so long will the public good that is money be captured to serve only the interests of the tiny, greedy minority in possession of private wealth."

- Ideal Money and Asymptotically Ideal Money - "[I]f we view money as of importance in connection with transfers of utility, we can see that money itself is a sort of 'utility', using the word in another sense, comparable to supplies of water, electric energy or telecommunications. And then, if we think about it, we can consider the quality of money as comparable to the quality of some 'public utility' like the supply of electric energy or of water."

[T]hose who control our money system escape close scrutiny. As a result too, there is widespread public ignorance of how the system for both creating and pricing money is effectively controlled not by central banks, but by the commercial banking system and by private, global capital markets. Despite all the hype around central bank decision-making, the public authorities have little impact on the management of the global financial system.

Perhaps one of the most disturbing aspects of academic neglect of money and monetary systems is the public’s failure to appreciate that the monetary systems of advanced economies evolved as a result of great struggles between private wealth and wider, democratic society. The success of these historic struggles meant that monetary systems in advanced economies evolved to become a great public good serving wider interests. However, periodically monetary systems are recaptured by the “robber barons” of private wealth, and then controlled and manipulated to serve their own rapacious greed.

- Where MMT Gets Its Accounting Wrong — And Right - "Start by thinking in terms of Household Net Worth. This measure has the virtue of encapsulating and telescoping all private-sector net worth, because households ultimately own firms, at zero or more removes, but firms don't own households (yet...)."

- United States' Net Wealth (Part 2) - "What does all this mean? Hmm. Not to easy to answer, except saying that familiarity with the system of measurement helps in understanding how the economy works."

- Translating 'net financial assets' - "I think the economy includes people who are already overinsured by their stock of net financial assets, and those people tend disproportionately to accumulate new issues. So we should think more about how we can accommodate private sector entities' need for some degree of insurance by redistributing existing net financial assets rather than creating new ones."

- Accounting as religion: Buffett, Derrida, and MMT - "The ability to pay taxes is a feature of money issued by sovereigns – a very important feature and part of how the government establishes its monopoly in the creation of money, but just because the government accepts money in payment for taxes (what else would they accept?) does not make the money they issue their 'liability.' "

- What's the obligation behind the Fed's 'liabilities'? - "[W]e accept paper money as payment/store of wealth because it is redeemable against our tax obligation as citizens."

- Market Macro Myths: Debts, Deficits, and Delusions - "In the context of the role that debts and deficits play in overall economic policy, in this paper I focus on the philosophy known as 'sound finance', which includes adherents who believe that governments should seek to balance their budgets. I, however, take a different view, and believe that the role of government when dealing with budget deficits should be one of 'functional finance', which ensures that the policies implemented help to reach the overarching goals of macroeconomic policy (generally held to be full employment and price stability)."

Myth 1: Governments are like households;

Myth 2: Printing money to finance budget deficits is inflationary;

Myth 3: Budget deficits/high debt lead to high interest rates;

Myth 4: Budget deficits are unsustainable;

Myth 5: Debt is a burden on future generations

Recently a friend said "just pay me back with cash" and I was confused because they actually meant "pay me back with Cash" which is an app with the worst name ever.

posted by miyabo at 5:35 AM on February 11, 2016 [8 favorites]

posted by miyabo at 5:35 AM on February 11, 2016 [8 favorites]

I guess we'll sit back and see how the Swedes do. I'd like to think that we'd move forward with digital currency in the US, but I just wrote a check with pen and paper to pay my landlord the other day. As in, 2016 "the other day". Oh, and there's also the issue that finance IT is the worst IT.

posted by indubitable at 6:44 AM on February 11, 2016 [1 favorite]

posted by indubitable at 6:44 AM on February 11, 2016 [1 favorite]

On reading further, the comparison to telcos and cable companies is apt.

posted by indubitable at 6:46 AM on February 11, 2016

posted by indubitable at 6:46 AM on February 11, 2016

Great post. Hours of entertainment.

posted by aspersioncast at 8:36 AM on February 11, 2016

posted by aspersioncast at 8:36 AM on February 11, 2016

Hours of entertainment.

Bitcoin threads always are. It seems to be a general rule that the greater the hype about the inevitability of the glorious Bitcoin future, the larger and more embarrassing the subsequent Bitcoin-related scandal or scam is. I wonder what we have to look forward to in the coming months.

posted by Sangermaine at 8:44 AM on February 11, 2016 [1 favorite]

Bitcoin threads always are. It seems to be a general rule that the greater the hype about the inevitability of the glorious Bitcoin future, the larger and more embarrassing the subsequent Bitcoin-related scandal or scam is. I wonder what we have to look forward to in the coming months.

posted by Sangermaine at 8:44 AM on February 11, 2016 [1 favorite]

No thank you. I will keep using cash as long as it is available, because I don't trust any of the people keeping digital records to act in my best interests. Not only that, I believe it is reasonable to assume, at this point, that I am nothing to them but an exploitable resource, and would therefore prefer to deny them as much leverage as possible, even when it makes my life a little less convenient.

That said, this is one of the most informative posts I have ever seen, and I look forward to reading through the links and learning something about the future of money.

posted by Mars Saxman at 9:54 AM on February 11, 2016 [1 favorite]

That said, this is one of the most informative posts I have ever seen, and I look forward to reading through the links and learning something about the future of money.

posted by Mars Saxman at 9:54 AM on February 11, 2016 [1 favorite]

Bitcoin threads always are.

it's not really about bitcoin tho or even blockchains; it's thinking about electronic payments more generally -- which btc has certainly helped bring attention to and catalyze developments in -- and the legal/technical challenges to its adoption; what's interesting to me is whether an 'internet of money' will be as transformative to finance (law and accounting) as it has been for media... and its impact on gov't :P

like consider GNU/Taler -- helped brought to you by mefi's own jeffburdges! -- which isn't blockchain based, and then maybe look backwards: "West tells his nightmare of return to the 19th century to Edith, who is sympathetic. West's citizenship in the new America is recognized, and he goes to the bank to obtain his own account, or 'credit card', from which he can draw his equal share of the national product."

posted by kliuless at 10:40 AM on February 11, 2016 [2 favorites]

it's not really about bitcoin tho or even blockchains; it's thinking about electronic payments more generally -- which btc has certainly helped bring attention to and catalyze developments in -- and the legal/technical challenges to its adoption; what's interesting to me is whether an 'internet of money' will be as transformative to finance (law and accounting) as it has been for media... and its impact on gov't :P

like consider GNU/Taler -- helped brought to you by mefi's own jeffburdges! -- which isn't blockchain based, and then maybe look backwards: "West tells his nightmare of return to the 19th century to Edith, who is sympathetic. West's citizenship in the new America is recognized, and he goes to the bank to obtain his own account, or 'credit card', from which he can draw his equal share of the national product."

posted by kliuless at 10:40 AM on February 11, 2016 [2 favorites]

When there's no more cash, what will beggers collect?

posted by tspae at 11:45 AM on February 11, 2016

posted by tspae at 11:45 AM on February 11, 2016

kliuless, I have no time right now to read this post, but I just wanted to say: spectacular job

posted by His thoughts were red thoughts at 1:40 PM on February 11, 2016

posted by His thoughts were red thoughts at 1:40 PM on February 11, 2016

I'm one of the olds, so I'll just say that there was a brief episode about 30 years ago when I was in a queue in a variety store behind a drug-addled person wearing expensive clothes trying to pay for a chocolate bar with a credit card, which was a rather unusual thing at that time. Complications ensued. This imprinted upon my mind at that time that not using cash for small trivial purchases was a sign of decadence. Obviously the world has changed around me since then.

posted by ovvl at 5:42 PM on February 11, 2016

posted by ovvl at 5:42 PM on February 11, 2016

“The business model of Wall Street is fraud”? Kind of - "The basic problem is that almost all of what we think of as [private] 'money' — deposits, money-market mutual funds buying commercial paper, repos, whatever — is really short-term debt. Banks offer total safety to depositors (and repo counterparties, etc, but for our purposes these are the same thing) even though the assets backing these liabilities are often tough to value, vulnerable to losses, and difficult to sell in a pinch. The mismatch between the advertised 'safety' of bank debt and the riskiness of bank assets is what makes the industry profitable and its employees so well-paid."

Beneficiary of rent extraction says rents explain inequality - "The International Monetary Fund has estimated that the big US banks received possibly more than all of their profits from the implicit subsidies associated with being 'too important to fail', as opposed to actually producing anything of value." (viz. cf.)

How negative is negative? Try 4.5 per cent negative

posted by kliuless at 1:11 PM on February 12, 2016 [1 favorite]

Beneficiary of rent extraction says rents explain inequality - "The International Monetary Fund has estimated that the big US banks received possibly more than all of their profits from the implicit subsidies associated with being 'too important to fail', as opposed to actually producing anything of value." (viz. cf.)

How negative is negative? Try 4.5 per cent negative

First a quick summary: Negative rates might be destroying the banking system. They might, as Kocherlakota says, be "a sign of a terrible policy failure by fiscal policymakers." They might simply be a experiment being played out in real time which we are as yet unfit to judge.Narayana Kocherlakota Argues That Negative Interest Rates Should Be Seen as Part of Conventional Monetary Policy - "He thinks there is some limit below which interest rates cannot go, because of paper currency. But the paper currency problem is well on its way to being solved: Electronic Money."

They might also get a lot... more.

We've looked at the idea of a lower bound based on storage costs, utility costs etc before but now JPM are saying it is really around 4.5 per cent (in Europe with caveats and a little more restrained elsewhere) since the incentive to move into cash is being managed by tiered deposit rates.

posted by kliuless at 1:11 PM on February 12, 2016 [1 favorite]

-Why Wall Street Is Embracing the Blockchain—Its Biggest Threat [1,2]

-Why the system needs liquidity savings before it can end QE

-Banks are still the weak links in the economic chain

kocherlakota's replacement...

-Break up the banks, says Minneapolis Fed chief

-Kashkari suggests either 1) breaking up TBTF banks, 2) raising capital requirements, and/or 3) taxing leverage

also btw on NIRP...

-End the negative-rate negativity

-Yup, negative rates were a really bad idea [1,2]

posted by kliuless at 6:54 PM on February 17, 2016 [1 favorite]

-Why the system needs liquidity savings before it can end QE

-Banks are still the weak links in the economic chain

kocherlakota's replacement...

-Break up the banks, says Minneapolis Fed chief

-Kashkari suggests either 1) breaking up TBTF banks, 2) raising capital requirements, and/or 3) taxing leverage

also btw on NIRP...

-End the negative-rate negativity

-Yup, negative rates were a really bad idea [1,2]

posted by kliuless at 6:54 PM on February 17, 2016 [1 favorite]

I'm really not sure why you would discuss MMT without linking to the literature out of UMKC.

posted by wuwei at 7:03 AM on February 19, 2016

posted by wuwei at 7:03 AM on February 19, 2016

oops, MMT Primer by l.randall wray (previously ;)*

oh and...

oh and...

- Stephanie Kelton's appointment is a BFD: 'Bernie Sanders named University of Missouri - Kansas City professor Stephanie Kelton as his chief economist for the Senate Budget Committee'*

- We need Bubbles: "We become wealthier when we create money out of thin air, not poorer."

- 'Helicopter money' on the horizon, says Ray Dalio: "The Bridgewater founder says this third era of monetary policy will range from central banks directly financing government spending through electronic money-printing to what the famous economist Milton Friedman coined 'helicopter money' in 1969, in other words central banks disbursing cash directly to households."

- Timid central bankers have failed to convince sceptical audiences: "central bankers tend not to adopt major shifts in mandates and targets unless urged to do so by popularly elected governments. It is difficult to muster Rooseveltian resolve without a Roosevelt."

- Faster Growth IS Possible - And It May Well Be Desirable: "To sum up: above-normal growth is always possible. The current data on market prices like interest rates and wages suggest that above-normal growth might well be desirable. The ongoing constraints on monetary policy suggest that we can best achieve that faster growth through demand-oriented policies."*

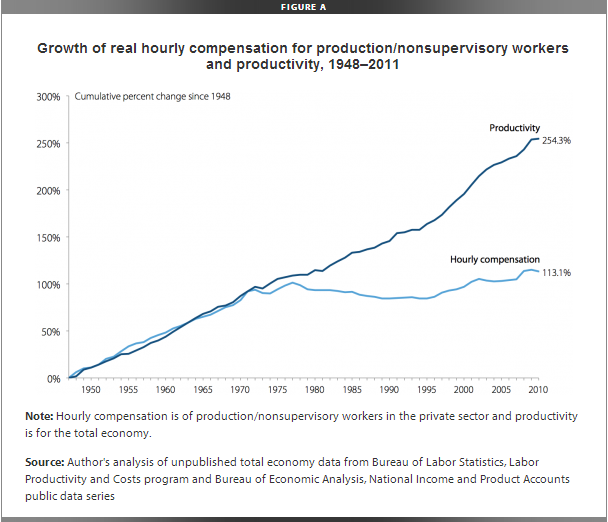

- How Cheap Labor and Capital Suggest that Faster Growth is a Great Deal: "This picture is key in understanding the opportunities that may be available. It depicts the evolution of labor share - the ratio of real wages to average labor productivity - in the nonfarm business sector. This ratio remains low by historical standards. The low level suggests that, for whatever reason, labor is unusually cheap... The prospect of higher demand could lead to more innovation and faster total factor productivity growth over this period. I argue here that we saw exactly that kind of effect from anticipated higher demand in the Great Depression. Such an effect would make faster growth an even better deal."

- NIRP Special Edition: "Here's an example of how negative rates can cause some weirdness. The policy can lead to some odd phenomena. Eva Christiansen, a Danish sex therapist, last year signed a three-year business loan with a negative interest rate, which in practice meant the lender had to pay her about DKr7 ($1) a month — vividly underscoring how the experiment can hurt banks."

{kind=link}

« Older for multiple meanings of 'Hack' | Herland Newer »

This thread has been archived and is closed to new comments

In the meantime, from the Moneyness link:

> People seem more intent on hoarding the stuff than trading it around in the "ordinary course of business."

People still talk about the "value" of bitcoin in terms of dollars, as if it's a good, rather than currency.

When goods are denominated in bitcoins, then it'll be currency.

Also, talking about the functions of money as what makes it "unique" seems strange to me. Rather, comparing any putative money system against how well it satisfies these functions serves as a measure not of whether it is "unique" (a concept that doesn't admit to degree) but how well it works as money. In other words, store of value, unit of account, medium of exchange, combine to form a definition of ideal money.

Fungibility goes to how well it serves these functions, mostly as a medium of exchange and unit of account.

posted by one weird trick at 3:21 AM on February 11, 2016 [1 favorite]